Your credit report contains detailed information about your credit history. Essentially, the information in your report provides an overview of your credit history and credit health. Plenty of details are included in your credit report that have a direct impact on your credit score calculation, including public records.

So, what exactly are public records on credit reports, and how do they affect your credit health?

Key Points

- Public records are items in your credit report that are tied to local, federal, and municipal governments and are a matter of public record.

- Examples of public records include bankruptcies, consumer proposals, and liens.

- Public records can have a negative effect on your credit score.

What Is A Public Record?

A public record is any municipal, provincial, or federal documentation that is accessible to the general public. Broadly speaking, public records refer to all legal and government matters. There are several types of public records that can be noted on your credit report, including the following:

Bankruptcies

Bankruptcy is a legal procedure in Canada that absolves you of most of your debt. However, you may lose your assets in the process, depending on your specific situation.

Bankruptcy is filed through a Licensed Insolvency Trustee and is considered a last resort. When you file for bankruptcy, the credit bureaus will be notified and it will become part of the public records. These records will be accessible to anyone who wishes to see it.

Consumer Proposals

A consumer proposal is another legal process that can absolve you of your debts. However, your debt should be no more than $250,000 and you must have the financial capability to repay a percentage of your debts.

Consumer proposals generally last between 2 to 5 years. Like bankruptcy, this program is filed through a Licensed Insolvency Trustee and will be reported to the credit bureaus. This information will also become part of the public records and will be accessible to anyone who requests it.

Debt Management Programs

A Debt Management Program (DMP) is a debt relief solution for those who need a bit of assistance managing their debt. With a DMP, you consolidate your debts into one affordable payment; however, you’ll still be paying all of your debt.

Unlike a consumer proposal, your debt isn’t reduced, but rather your interest charges may stop and you may be given more time to pay off your debt. DMPs will show up in the public records of your credit report.

Liens

A lien is a term used to define an asset that is used as security for a loan, like a personal loan or a mortgage. When these go unpaid, the lenders have the right to seize the asset to recoup any losses.

Tax liens, judgment liens, and real estate liens are some of the types of liens that can show up on your credit report under the public records section.

Do note, that non-financial public records will not be shown on your credit report. For example, a divorce is a public record, but it will not show on your credit report.

Where Do Public Records Appear On Your Credit Report?

Public records are typically listed in a dedicated section of your credit report, separate from your credit accounts and inquiries. Depending on the credit bureau, the layout of the credit report may vary slightly, but public records are generally grouped under headings such as the following:

- Public Records

- Legal Items

- Collections & Legal Filings

| Note: Since this section is highly visible to lenders, even one entry can significantly impact lending decisions. |

How Is Your Credit Score Affected By Public Records?

Public records can have a negative effect on your credit score. When it comes to calculating your credit score, a handful of key factors are used, including public records.

Generally speaking, public records account for roughly 10% of your credit score calculation. So, if you have public records noted on your credit report, they will be factored into your credit score calculation. As such, your credit score could be negatively impacted.

Other factors that are used to calculate your credit score include:

- Payment History

- Credit Utilization

- Age Of Credit History And Accounts

- New Credit

How Do Lenders Interpret Public Records?

Lenders don’t just look at your credit score. They also assess the type, severity, and date of public records. Here are a few examples:

- Recent bankruptcies signal higher risk than older ones nearing removal

- Paid judgments may be viewed more favourably than unpaid ones

- Consumer proposals can indicate debt management efforts versus default

In mortgage underwriting, public records can impact the following:

- Loan approval eligibility

- Interest rates

- Down payment requirements

This makes context and timing just as important as the public record itself.

How Long Does A Public Record Remain On Your Credit Report?

Public records can remain on your credit report for three to 10 years, depending on the exact record type1. While public records can stay on your credit report for a long time, the impact it generally has fades with time. Moreover, they will eventually be removed from your credit report.

The following chart lists various public records and how long each can remain on your credit report:

| Remark | Equifax | TransUnion |

| Bankruptcy | 6 years after the date of discharge | 6 years after the date of discharge in all provinces except: -Ontario: 7 years -Quebec: 7 years -Newfoundland and Labrador: 7 years -PEI: 7 years |

| Multiple Bankruptcies | 14 years | 14 years |

| Consumer Proposals | 3 years after all debts are repaid, or 6 years from the filing date, whichever comes first | 3 years after all debts are repaid, or 6 years from the filing date, whichever comes first |

| Judgments | 6 years | 6 years in all provinces except: -Ontario: 7 years -Quebec: 7 years -Newfoundland and Labrador: 7 years -PEI: 10 years |

| Debt Management Plans | 2 years after debts are paid off | 2 years after debts are paid off |

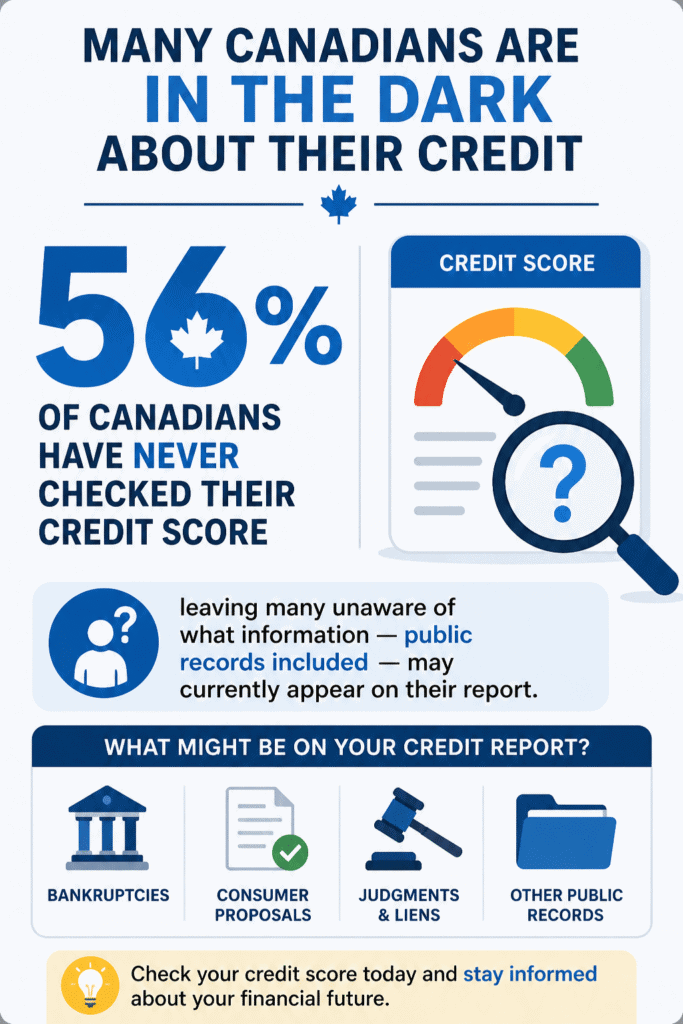

How Many Canadians Are In The Dark About Their Credit Reports?

Does Paying Off A Public Record Improve Your Credit Score?

Yes, but not immediately. Paying off debts tied to public records can prevent further legal action, improve how lenders perceive your risk, and stop additional penalties or interest.

However, the public record itself may still stay on your credit report for the full reporting period. That said, over time, its effect will gradually decrease, especially if you show positive credit behaviour afterward.

How To Improve Your Credit If You Have Negative Remarks In Your Public Records

If you continue to upkeep other aspects of your credit report and personal finances, the damage caused by items in your public record may not be as severe or long. To help boost your credit, here are a few things you can do:

Keep Up With Your Payments

Your payment history usually accounts for around 35% of your credit score calculation. This makes it the most significant factor in determining your credit score. As such, making your payments on time and in full is crucial.

Keep Your Credit Utilization Low

Also referred to as your debt-to-credit ratio, your credit utilization ratio measures how much of your available revolving credit you’re currently using compared to your total limit. This factor generally accounts for about 30% of your credit scores. Given that, it’s in your best interest to utilize your credit responsibly.

Most experts recommend using no more than 30% of your available credit for the most positive impact on your credit. So, if your credit card limit is $10,000, for instance, avoid spending more than $3,000 per month on credit.

Use A Secured Credit Card

If your public record is making it impossible for you to qualify for a credit card or loan, a secure credit card can help. They’re designed to help those with poor credit build a healthy credit score.

Secured credit cards work just like a regular credit card when it comes to making purchases. However, with a secured credit card, you have to provide a security deposit, which also acts as your credit limit. With every timely payment you make, you can steadily improve your credit score.

Avoid Applying For Too Many Credit Products

Applying for multiple credit products in a short period of time can hurt your credit. When you apply for a credit product, the lender will access your credit report, which will result in a hard inquiry. Multiple hard inquiries can negatively impact your credit scores and could signal to lenders that you’re having financial difficulties.

So, it’s in your best interests to avoid taking out too many loans or credit products if your goal is to build good credit.

| Remember: Consistency is key. Many consumers begin seeing credit score improvements within 12 to 24 months of responsible behaviour2. |

How To Manage Public Records On Your Credit Report

As mentioned, public records can hurt your credit score. But there are things you can do to minimize their impact.

Keep Tabs On Your Credit Report

It’s recommended that you check your credit report on a regular basis to make sure the information contained within them is entirely accurate. You can get a free copy of your credit reports from the credit bureaus. Look through your report to see if there are any mistakes.

Dispute Mistakes

If you notice that there are notes of public records that are in error, you can file a dispute with the credit bureau. To support your claim of inaccuracy, you may need to provide documentation to help the bureau correct any mistakes found on your credit report.

Pay Your Debts

If there is a public record noted on your credit report that is a result of an unpaid debt, like a tax lien or judgment, pay it off in full as soon as you can. Doing so can help improve your credit score.

Bottom Line

If your credit report contains public records, your credit score could take a hit, but not forever. Over time, the impact of a public record on your credit score will diminish until the remark falls off your report. With continued responsible management of your personal finances, you can steadily rebuild your credit profile, despite a past of public records on your credit report.

FAQs

Do all public records show up on your credit report?

Why is there a public record on my credit report?

Can I have a public record removed from my credit report?

Do public records affect mortgage approval in Canada?

Can employers see public records on your credit report?

References:

1Government of Canada. How long information stays on your credit report. Canada.ca

2Credit Canada. (2024, March 1). How Long Does It Take To Build Credit in Canada? CreditCanada.ca