When you decide to sell your home and buy a new one, it can be difficult to line up the closing dates for each transaction. Plus, many people rely on the proceeds from the sale of their current home to help pay for their new home. If you buy a new house before your current home closes, you could be left with two mortgages to carry. That’s where a bridge loan comes in handy.

Key Points

- A bridge loan is a short-term financing solution that homeowners may use to cover some of the costs of a new home purchase until their current home sale closes.

- This type of financing is designed to help homeowners avoid carrying two mortgages at once if they buy first while waiting for the closing date on their current home.

- Bridge loans can come with terms ranging from 90 days to 12 months, with interest rates that are often higher than typical mortgages.

- Once your current home closes, you can use the equity from the home to pay off the bridge loan.

What Is A Bridge Loan?

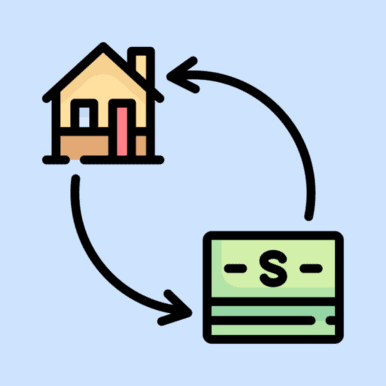

A bridge loan is a temporary financing solution meant to help homeowners avoid carrying two mortgages when there’s a gap between the closing date of their current home and their new home purchase. Essentially, this type of loan “bridges” this gap between the two transactions.

Bridge loans work by allowing homeowners to access their home equity for the down payment on their new home while they wait to sell their current home.

Bridge Loan Features

Bridge loans are typically characterized by the following:

- Term Length – Bridge loans are short-term loans that range from 90 to 120 days, though they can be as long as 12 months or more.

- Interest Rates – Interest rates on bridge loans are typically higher than regular mortgages.

- Repayment – No payment is required until your current home is sold, at which point you can use the proceeds to pay off your bridge loan.

How Does Bridge Financing Work?

A bridge loan works as follows:

Step 1. Show Your Lender Both Firm Offers

Your lender will need to see that both your existing home and new home have been sold firm. That means you’ll need to show your lender a copy of the purchase agreement for both your existing home and your new home.

Step 2. Use The Bridge Loan To Help Finance Your New Home Purchase

A bridge loan allows you to access equity in your existing home to fund the down payment on your new home. This will allow you to carry both mortgages until the sale of your current home closes.

Step 3. Pay Off Your Bridge Loan Once Your Current Home Closes

When your existing home sale closes, you can use the proceeds from the sale to repay the bridge loan.

How Much Can You Borrow?

When you apply for a bridge loan, your lender will assess how much they can lend you. However, the amount you can qualify for depends on the equity in your home. Generally speaking, you may qualify for up to the value of your home, less your outstanding mortgage balance.

For example, if you owe $350,000 and your home is valued at $500,000, then you could be eligible for $150,000 ($500,000 – $350,000). The lender will also subtract the closing costs from your bridge loan amount.

When Do You Repay The Bridge Loan?

Once your current home has been sold, the proceeds from the sale can be used to pay off the bridge loan. If you’re unable to close on the sale of your home before the bridge loan term ends, you’ll be responsible for your current mortgage payments, the mortgage on your new home, and the bridge loan.

Where Can You Get A Bridge Loan In Canada?

Depending on your financial health and the equity in your home, you may be able to get a bridge loan from a bank, subprime lender, or private lender.

Banks

Many banks and other traditional financial institutions offer bridge loans. However, they often have strict approval requirements that borrowers must meet. This can make it difficult for individuals with bad credit to qualify for a bridge loan. Generally, banks will look at the borrower’s credit score, income, debt-to-income (DTI) ratio, employment, and home equity.

Credit Unions

Credit unions are major financial institutions, but most are not federally regulated. As such, they typically have more relaxed lending requirements. Given this, you may have better luck getting a bridge loan with these types of lenders compared to banks.

Subprime Lenders

Also known as ‘B’ lenders, subprime lenders are those that serve “subprime” borrowers, or those with low income or problematic DTI ratios. They’re more lenient with their loan criteria, though they still require borrowers to meet certain requirements. As such, subprime lenders may be more willing to offer bridge loans to homeowners with lower credit or higher DTI ratios.

Private Lenders

Many private lenders also offer bridge loans. Private lenders are not federally regulated and are not required to subject their clients to the same strict loan criteria as traditional lenders.

When it comes to bridge loans, private lenders have less stringent loan requirements. These private lenders are often the best choice for those with poor finances and low credit scores.

Pros And Cons Of Bridge Financing

Bridge financing can certainly be helpful, but it comes with some drawbacks that you should consider:

Pros Of Bridge Financing

The following are some advantages of bridge financing:

- Fast Access To Cash. A bridge loan provides borrowers with quick cash they can use to help them purchase their new home.

- Bridges The Financing Gap. Coordinating the closing dates on the sale of your current home and the purchase of a new home can be difficult. A bridge loan can be beneficial if you plan on using the proceeds from the sale of your current home to help finance your new home. With a bridge loan, you can get the funds you need to buy a new home without first having to close on your current home.

- Lower Requirements. Bridge loans typically have easier requirements than a regular mortgage. Most lenders mainly require a copy of the Sale Agreement and the Purchase Agreement, as well as a certain amount of equity in your home.

Cons Of Bridge Financing

Along with the perks of bridge financing come a handful of drawbacks:

- Expensive. Bridge loans typically have higher interest rates than a regular mortgage.

- Requires Equity. To get a bridge loan, you need a significant amount of equity in your home. The exact amount of equity required will depend on the lender.

- Potentially Two Mortgages At Once. If the sale of your current home falls, you’ll be stuck with two mortgages and a bridge loan. Even worse, the lender could seize your home if it collateralized the bridge loan and you’re not able to pay the loan on time.

When Can A Bridge Loan Work For You?

Bridge loans can be a good option if:

- You need financial help with the down payment for the new home. Sellers typically use the proceeds of their sale to put toward the purchase of their next home. However, if you haven’t closed your current home, you can use a bridge loan to access those funds earlier.

- You Need To Act Fast. If you’ve found a great house and don’t want to lose it (especially in a hot market), a bridge loan can provide you with the funds to carry through with the transaction.

- Your Closing Date Is Not Aligned. If the closing dates on the two homes don’t align, a bridge loan can help bridge the gap.

- The Seller Won’t Accept Your Conditions. If you make an offer on a house that includes selling your house as a condition, some sellers may reject your offer. A bridge loan will allow you to buy the house before your home sells.

Alternatives To Bridge Loans In Canada

As mentioned, a bridge loan allows you to access your home’s equity to cover the down payment on your new home until the sale of your existing home closes. However, there may be other ways to access your home equity to help you fund your new home purchase.

Home Equity Line Of Credit (HELOC)

If you have enough equity in your current home, you can access it using a HELOC to put toward your down payment on your new home. With a HELOC, you can access up to 65% of your home’s value. You’ll be given access to a revolving line of credit up to a certain limit, which you can draw from as needed.

If you choose this option, you’ll need to apply for the HELOC and tap into your equity before you sell your current home.

Home Equity Loan

Like a HELOC, a home equity loan allows you to tap into your home equity. With a home equity loan, you can access up to 80% of your home’s value.

Unlike a HELOC, a home equity loan provides you with a lump sum of money, which you can use to put toward your down payment on your new home. You then repay the loan via regular installments over a set term.

Bottom Line

A bridge loan is a great financial tool to use if you’re buying and selling at the same time. More specifically, it can keep you out of financial trouble if you buy a new home before your current home sells.

Bridge Financing FAQ

What do I need to qualify for bridge financing?

Does bridge financing require a deposit?

Can I get a bridge loan if I have bad credit?

Can I secure a bridge loan if I still need to sell my current home?

How long do I have to pay off my bridge loan?

Will bridge financing hurt my credit score?

- Rules For Buying A Second Home And Renting Out The First In Canada

- Can You Pay Your Mortgage With A Credit Card?

- What Is A Home Builders Mortgage?

- Can You Use Rental Income To Qualify For A Mortgage In Canada?

- Down Payment Assistance Programs In Canada

- How To Borrow Using Your Home Equity

- Minimum Credit Score For A Mortgage In Canada (2026)

- How Much Does A $300,000 Mortgage Cost In Canada?

- What Is A Purchase Plus Improvements Mortgage?

- Bi-Weekly Payments vs. Monthly Mortgage Payments

- Cosigning On A Mortgage: Things You Need To Know

- Spousal Buyout Of A Mortgage In Canada

- How To Get A Farm Mortgage

- The Costs Of Owning A Home In Ontario: A Complete Guide

- The Canadian Mortgage Stress Test In 2026: How It Works And How To Pass It

- Your Guide To Gifted Down Payments In Canada

- How To Remove A Name From A Property Deed

- No Down Payment Mortgages In Canada: A Guide

- A Guide On How To Buy A Foreclosed Home In Canada

- How To Borrow Money For A Down Payment