When your debt is sold to a collection agency in Canada, it can feel intimidating. But knowing what actually happens can help reduce the stress from the process. If your lender sells your unpaid account to a collection agency, the collector becomes responsible for contacting you, negotiating payment, and reporting the debt to the credit bureaus. This can affect your credit, your rights, and the way you handle repayment, so understanding the steps ahead can help you stay informed and in control.

Key Points:

- Debts may be sent to collections after 90 days of missed payments

- The agency must notify you in writing, and may contact you to verify the debt.

- They may also pursue legal action if unpaid.

- A debt in collections can severely damage your credit score (R9 rating) and remain on your report even after repayment.

- You can dispute the debt, negotiate repayment, or face consequences like wage garnishment if the issue isn’t resolved.

What Happens If Your Debt Is Sold To A Collection Agency In Canada?

If a collection agency takes over your debt, they are required by law to notify you before they come after you to collect what you owe. The notification should be in writing and should be sent to you within 5 days of the agency’s attempt to get in touch with you.

The notice should include the following information:

- The debt collection agency’s name

- The name of the business or individual you owe money to

- The amount owed

- A statement of your right to dispute the debt

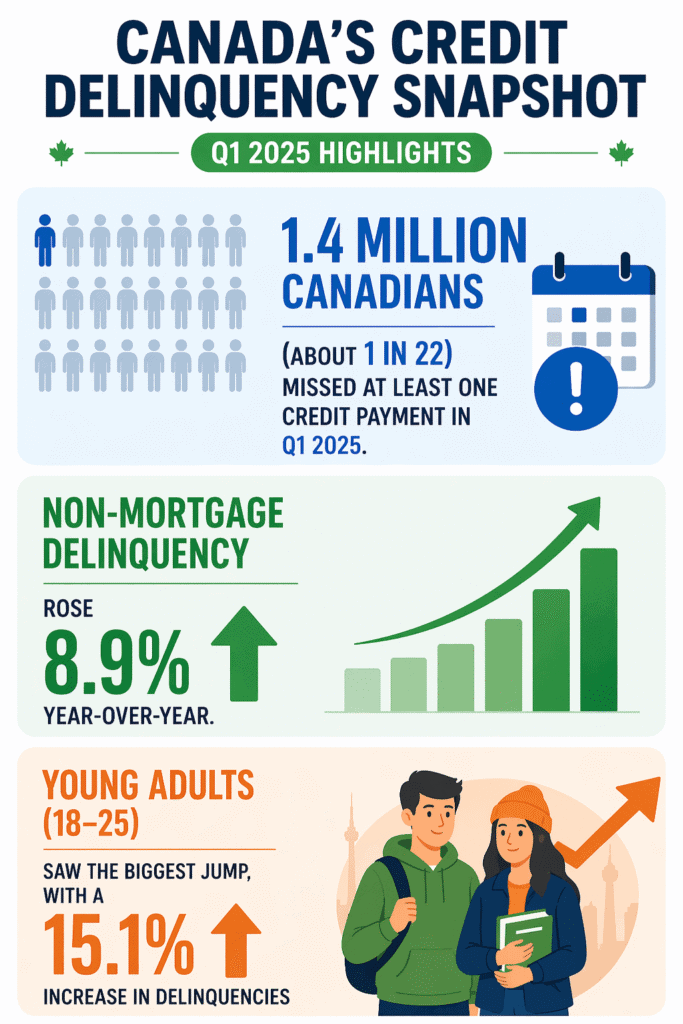

What Do Credit Delinquencies Look Like In Canada?

How Does Debt Collection Agency Work In Canada?

The debt collection process may work slightly differently from one province to the next. That said, the general process typically involves the following steps:

Step 1: Contact From The Debt Collection Agency In Writing

As mentioned, you should first receive a written notice from the debt collection agency. The letter will request that you continue repaying what you owe and notify you of the agency’s intent to collect your outstanding debt.

Step 2: Contact From The Agency Via Telephone

Legally, debt collectors are allowed to call you 5 days after they send you a written notification. If they cannot get a hold of you because you’ve changed your phone number or address, they are legally permitted to reach out to your family, friends, and employer.

However, they can only contact them to obtain your phone number or address.

You may try to ignore collection calls in an effort to avoid dealing with the agency, but they can be persistent and will likely make repeat calls if you don’t answer. Eventually, they may try other avenues to collect what you owe, including taking you to court.

Step 3: Debt Collection Agency Will Provide You With Proof Of Debt

When the debt collection agency finally makes contact with you, they must provide you with evidence of the outstanding debt you still owe. More specifically, they’ll need to provide you with the following information in writing:

- The name of the collection agency

- The original creditor

- The date that the debt was transferred to the collection agency

- The amount you owe

Step 4: Repay The Debt You Still Owe

Once you’ve been provided with all the required information about your debt, you’ll need to find a way to pay it back. If you’re unable to pay the entire amount back right away, explain your situation to your debt collector and offer up an alternative solution to avoid any further or more aggressive debt collection actions.

Step 5: Debt Collection Agency May Make A Legal Request For Repayment

If you’re unwilling to pay back the debt you owe, the debt collection agency may attempt to get you to settle your account by taking legal action.

If you don’t pay back your debt, you may be subject to litigation if the agency believes it will help them collect. They must provide you with at least 21 days’ notice in advance of legal action.

Step 6: Court Hearing And Repayment

You’ll need to attend a court hearing if the debt collection agency takes legal action against you. If the judge determines that you are required to repay the amount the debt collection agency is suing you for, a judgment may be signed that will require you to legally pay off your debt.

With a judgment signed by the court judge, your debt collector has the authority to garnish your wages as a means to satisfy the debt owed. Otherwise, you may have to file for bankruptcy or a consumer proposal to get out of the debt, which can have significant consequences on your credit.

What Types Of Debt Can Be Sold To Collections?

Many types of consumer debt can be sold to collection agencies, including the following:

- Credit card balances

- Personal loans

- Lines of credit

- Payday loans

- Utility bills

- Medical-related debts

How Long Can A Collection Agency Try To Collect In Canada?

Collection agencies are limited by the “statute of limitations,” which varies by province.

The statute of limitations for debt collection in Canada is the legal time limit for how long a creditor or collection agency can sue you for an unpaid debt. After this period expires, the debt still exists, but you’re protected against being taken to court for the debt. In many provinces, including Ontario, this period is typically 2 years from the date of your last payment or acknowledgment of the debt.

However, even after this period expires:

- The debt doesn’t disappear

- Collectors may still contact you (with restrictions)

- The debt may remain on your credit report for up to 6 to 7 years

This is why understanding timelines is crucial when deciding whether to repay, negotiate, or dispute a debt.

What Should You Do If Your Debt Is Sold To A Collection Agency In Canada?

Depending on whether or not your lender has already sold your debt to a collection agency, here’s what you can do:

Your Lender Is Planning On Selling Your Debt To A Collection Agency In Canada

If you find out that your creditor plans to transfer your debt to a collection agency, you should get in touch with your creditor immediately to see if you can work out an arrangement to settle your debt.

You may negotiate with the creditor to pay either some or all of what you owe to avoid collections. You may also be able to make alternative arrangements with the creditor to repay your debt.

Your Lender Has Sold Your Debt To A Collection Agency

If the debt has already been transferred to a debt collection agency, you have some options:

- Dispute the debt. If you don’t believe you’re obligated to pay the debt, you have the right to dispute it.

- Make sure the collection agency follows the same rules as your original creditor when collecting the debt. The new creditor is not allowed to add any additional interest or fees to your debt. However, they are given specific permission to do so according to the terms of the original debt agreement.

- Pay the debt. If your debt is sold to a debt collection agency, you will owe the new creditor money. If you choose not to dispute the debt, you’ll need to repay the debt to avoid being taken to court or having your wages garnished.

Can You Negotiate Or Settle Collection Debt?

Yes, many collection agencies are willing to negotiate settlements1. This means you may be able to pay less than the full amount owed.

Common strategies include the following:

- Offering a lump-sum settlement for less than the balance

- Setting up a structured payment plan

Before agreeing to anything, always get the terms in writing. This protects you and ensures the agreement is honoured.

What Happens To Your Credit If Your Debt Is Sold To A Collection Agency In Canada?

Your credit score can take a hit if your debt is transferred to a collection agency. The debt will show up on your credit report as outstanding debt that has not been paid and has gone to collections.

When this happens, you’ll receive a credit rating of R9, which is the lowest credit rating you can receive.

Payment history is the most important factor in your credit score. A history of missed debt payments can also have a negative effect on your scores. Even if the debt collection agency gives up and stops calling you, the debt will still show up on your credit report, which can pull your credit score down.

Will A Debt Collection Be Removed From Your Credit Report If You Repay Your Debt?

It’s important to note that even if you fully repay the debt, the collection may still be recorded on your credit report, unless your creditor agrees to remove it.

How Will A Debt Collection Affect Me?

Debt collection can significantly negatively affect your credit. A low credit score can be detrimental to your financial and credit profile. You’ll have a tougher time getting approved for loans and credit products.

Even if you’re able to secure a loan, you may be charged higher interest, which will make your loans more expensive.

Low credit can also negatively impact your ability to get hired for a job, sign a lease, obtain insurance, or even sign a cell phone contract.

| How To Rebuild Your Credit After Collections Recovering from a collection account takes time, but it’s absolutely possible with the right strategy: – Make all future payments on time – Reduce your credit utilization below 30% – Consider a secured credit card to rebuild history – Avoid applying for too much new credit at once Over time, consistent positive behaviour can help offset the negative effect of collections on your credit profile. |

How To Avoid Debt Being Sent To Collections

It’s always better to prevent your debt being sent to collection than to deal with it afterwards. If you’re struggling financially, consider these steps early on:

- Contact your lender before missing payments

- Request payment deferrals or hardship programs

- Consolidate high-interest debt into one manageable payment

- Work with a credit counsellor for budgeting support

Taking action early can help you avoid long-term credit damage and collection activity altogether.

Who Can You Contact To Know More About Your Rights?

It’s important to understand your rights when your debt has been sent to collections. Debt collectors are not allowed to do any of the following:

- Contact anyone about information aside from your telephone number or address, with few exceptions.

- Call you on your cell phone, unless you give them that number.

- Contact your employer for any reason other than to verify your employment or obtain your telephone number or address.

- Contact you at your place of work, unless they don’t have your home number, they could not reach you at home, or you gave them permission to call you at work.

- Contact you on holidays, on Sundays (except from 1pm to 5pm), or on all other days from 9pm to 7am.

- Harass you by putting too much pressure on you, using abusive or threatening language.

- Lie about your debt situation.

- Add any costs to the debt owed other than legal fees or NSF fees.

To find out more about your rights when your debt has been sent to collections, you can call the federal Consumer Affairs office, or the office in your province or territory.

Provincial Consumer Affairs Offices

| Province | Phone Number | |

| British Columbia | 604‑320‑1667 Toll Free: 1‑888‑564‑9963 | info@consumerprotectionbc.ca |

| Alberta | 780‑427‑4088 Toll Free: 1‑877‑427‑4088 | service.alberta@gov.ab.ca |

| Saskatchewan | 306‑787‑5550 Toll Free: 1‑877‑880‑5550 | consumerprotection@gov.sk.ca |

| Manitoba | 204‑945‑3800 Toll Free: 1‑800‑782‑0067 | consumers@gov.mb.ca |

| Ontario | 416‑326‑8800 Toll Free: 1‑800‑889‑9768 Phone (TTY): 416‑229‑6086 Phone (TTY) 2: 1‑877‑666‑6545 | consumer@ontario.ca |

| Quebec | 418‑643‑1484 Toll Free: 1‑888‑672‑2556 | N/A |

| New Brunswick | 1‑866‑933‑2222 | info@fcnb.ca |

| Nova Scotia | 902‑424‑5200 Toll Free: 1‑800‑670‑4357 | askus@novascotia.ca |

| Newfoundland & Labrador | 709‑729‑2600 Toll Free: 1‑877‑968‑2600 | consumeraffairsaccount@gov.nl.ca |

| Prince Edward Island | 902-368-4550 Toll Free: 1‑800‑658‑1799 | ccs@gov.pe.ca |

| Yukon | 867‑667‑5111 Toll Free: 1‑800‑661‑0408 (ext 5111) | consumer@gov.yk.ca |

| Northwest Territories | 867‑767‑9161 (ext. 21022) | consumer_affairs@gov.nt.ca |

| Nunavut | 867‑793‑3303 Toll Free: 1‑866‑223‑8139 | consumerprotection@gov.nu.ca |

| Federal | 1‑800‑328‑6189 | N/A |

Bottom Line

When taking out a loan or line of credit, you make a promise to a lender to pay back the entire amount loaned, plus interest. If you’re having trouble paying back your loan, be sure to contact your lender to try to find a solution. You can also contact a credit counsellor to help you manage your debt and explore different debt relief options.

FAQs

Why do banks use collection agencies?

What is a collection agency?

How do collection agencies make money?

What are your rights with a collection agency?

How should I deal with a collection agency?

References:

1Hoyes Michalos. Can I Negotiate a Debt Settlement on My Own? Hoyes.com