Knowing where your credit falls on the credit score range is important. Depending on your score and ranking, you may receive lower interest rates and may be more likely to be approved for loans and other credit products.

Generally, a lender will look at both your credit report and your credit score in Canada, along with a variety of other factors (employment status, income, debt levels, etc.) to determine your creditworthiness. And since you’re the only one who can improve your credit scores, understanding your credit is that much more important.

Key Points

1. Credit scores in Canada range from 300 to 900 — the higher, the better.

2. A score of 660 or higher is generally considered good; anything below 560 is considered poor.

3. The average Canadian credit score is 679 as of 2026.1

4. You can check your score for free through Equifax, your bank, or a platform like CompareHub.

Credit Score Range Meaning In Canada

Credit Score Range Meaning

Move the slider to your score to see where it falls on the Canadian credit score range.

A score of 660–724 is considered good.

This information is for general guidance only. Credit scores can be interpreted differently by different lenders and credit bureaus, and your score is only one factor used in lending decisions.

What Is A Credit Score Range In Canada?

In Canada, credit scores range from 300 to 900. Where your score falls within that range helps lenders assess how risky it may be to lend to you. Generally, a higher credit score can improve your chances of approval and help you qualify for better interest rates and borrowing options.

Your credit score is generated using information in your credit report, which is maintained by Canada's two main credit bureaus, Equifax and TransUnion. However, lenders don't rely solely on your credit score. Many use their own scoring models and approval criteria, taking into account factors such as your income, existing debts, employment history, and overall financial profile.

It's important to remember that there is no universal standard for what each score means. Different lenders use different scoring models and approval criteria. For example, one lender may consider a score of 760+ excellent, while another may reserve that designation for scores of 780+. As a result, credit score ranges should be viewed as general guidelines rather than strict rules.

Credit Score Ranges In Canada

Here's how the credit score ranges break down in Canada, from poor to excellent. These ranges follow the Equifax model:

| Credit Score Range (Equifax) | Rating |

|---|---|

| 760–900 | Excellent |

| 725–759 | Very Good |

| 660–724 | Good |

| 560–659 | Fair |

| 300–559 | Poor |

Note: Equifax And TransUnion Use Different Ranges

The ranges above follow the Equifax model. TransUnion uses a different scoring model with different cutoffs, so the same number can carry a different label — a 768, for example, lands in "excellent" on the Equifax range but shows as "very good" on TransUnion's CreditVision score. This is also why your two scores won't always match.

What Is A Good Credit Score Range In Canada?

A good credit score in Canada is generally 660 or higher. Scores from 660–724 are considered good, 725–759 very good, and 760–900 excellent. At 660 and above, you'll qualify for most mainstream credit products, with the best rates typically reserved for scores above 725.

Want to know where the cutoff really sits? Here's a closer look at what makes a credit score good.

What Is A Bad Credit Score Range In Canada?

A bad credit score in Canada is generally below 560. Scores of 300–559 are considered poor, while 560–659 is fair. With a score in this range you can still borrow, but usually from alternative lenders and at higher interest rates. For example, here's what kind of loan you can get with a credit score of 450.

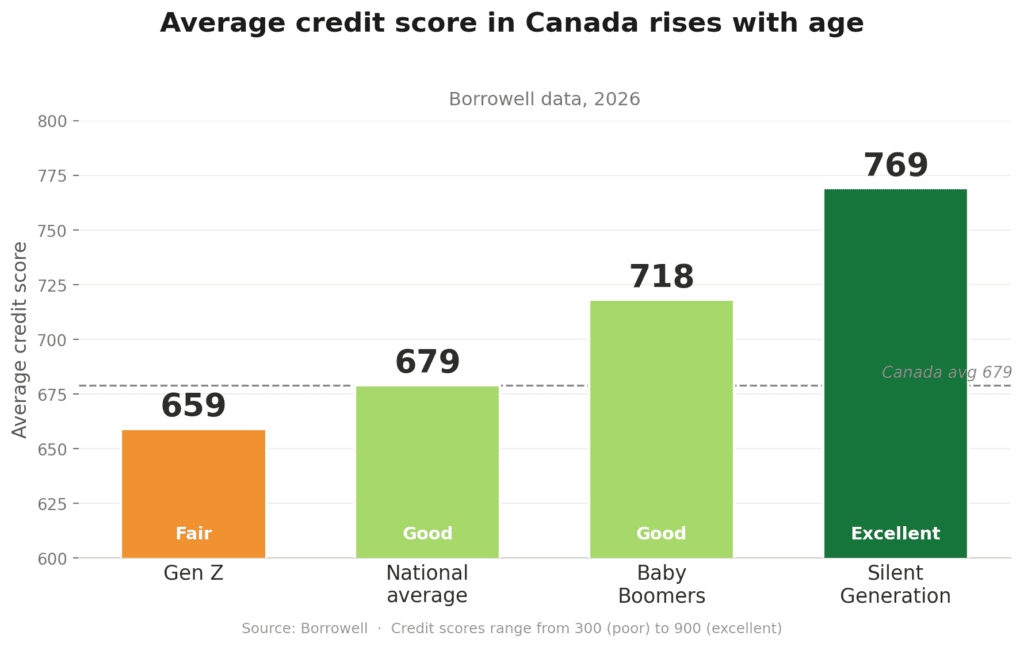

What Is The Average Credit Score In Canada?

The average credit score in Canada is 679 as of 2026, according to Borrowell.1 Averages tend to rise with age: Gen Z averages around 659, Baby Boomers around 718, and the Silent Generation around 769.1

Where you live matters too. See how you stack up by the average credit score by province and the average credit score in Canada by age.

Is 600 A Good Credit Score In Canada?

No, 600 is not a good credit score in Canada — it falls in the "fair" range (560–659). In practice, that means you can still get approved for some credit, but often at higher interest rates, with lower limits, and more often through alternative lenders than the big banks. The good news: 600 is only 60 points from the "good" range, so reaching 660 noticeably widens your options.

Keep in mind your score is only one factor — lenders also weigh your income, debts, and employment, so a strong overall profile can still earn an approval. Here's what a 600 credit score means for you.

Is 650 A Good Credit Score In Canada?

A score of 650 is fair — just below the "good" range that starts at 660. You can qualify for many products at 650, but you'll usually pay higher rates than someone in the good range, and the lowest mortgage rates or premium cards may be out of reach. A small push to 660+ can unlock meaningfully better pricing.

Remember, too, that your score is just one piece of the picture — your income, debt load, and history all factor into a lender's decision.

Is 700 A Good Credit Score In Canada?

Yes, 700 is a good credit score in Canada — it sits comfortably in the "good" range (660–724). With a 700, you'll qualify for most mainstream loans and credit cards at competitive rates, and you're well-positioned for mortgage approval. Climbing toward 725 ("very good") unlocks the best pricing lenders offer. That said, your score isn't the whole story — lenders still assess your income, existing debt, and job stability before approving you.

Learn more: 700 Credit Score

Is 800 A Good Credit Score In Canada?

Yes, 800 is an excellent credit score in Canada — it's in the top range (760–900). At this level you'll qualify for the best interest rates, the highest limits, and premium products, and approvals are rarely an issue on the credit-score front. A score of 780 is firmly excellent too.

Even so, an excellent score doesn't guarantee approval on its own — lenders still look at your income and debt levels — but it puts you in the strongest possible position.

Here's whether being in the 800 credit score club really matters, and what a credit score of 780 means.

How To Check Your Credit Score In Canada

You can check your credit score for free through the following sources:

Credit Bureaus

You can check your credit score through one of the two major credit bureaus in Canada: Equifax and TransUnion. Equifax provides credit scores for free to all Canadians, while TransUnion only offers free scores to Quebec residents. All others must pay a monthly subscription fee to access their TransUnion credit score.

Big Banks

All five of Canada’s Big Banks — including RBC, Scotiabank, TD Bank, BMO, and CIBC — allow clients to check their credit scores for free.

Online Third-Party Platforms

You can also access your credit scores and credit report for free third-party service providers like Loans Canada’s Compare Hub, Borrowell and Credit Karma.

| Cost | Credit Score | Credit Report | ||

| Free | Yes | Yes | Visit Site |

| Free | Yes | Yes | Visit Site | |

| Free | Yes | Yes | - |

Why Is My Credit Score Different?

You don't have just one credit score. Equifax and TransUnion each calculate their own, and they may differ because lenders don't always report to both bureaus, and each bureau may have slightly different information on file. The scoring model used also matters — the score your bank shows you can differ from the one a lender pulls.

This is normal. What matters is that your scores sit in roughly the same range and trend in the same direction over time.

What Factors Affect Your Credit Score In Canada?

Your credit score is calculated from five main factors, each carrying a different weight:2

The 5 Factors That Make Up Your Credit Score

Payment History (~35%)

Whether you pay your bills on time. The single biggest factor in your score.

Debt-To-Credit Ratio (~30%)

How much of your available credit you're using. Keeping it under 30% helps.

Length Of Credit History (~15%)

How long your accounts have been open. Older is better.

Public Records (~10%)

Bankruptcies, collections, and other negative records drag your score down.

Credit Inquiries (~10%)

Too many hard inquiries in a short window can lower your score.

How To Improve Your Credit Score Range In Canada

As mentioned, many factors can affect your credit scores. Working on improving those factors can help improve your credit score. Similarly, here are a few other things you can do to help improve your credit score range:

- Remove Errors On Your Credit Report – Errors on your credit report can cause your credit score to be lower than it should be. Check your credit report, and having any errors rectified may help your credit score bounce back up.

- Don’t Apply For Too Many Credit Products – When searching for a loan or credit card, it’s important to limit the number of credit applications you submit. Too many within a short period of time can negatively affect your credit scores. This is because each credit application generally requires a hard credit check, which can hurt your credit scores.

- Use A Secured Credit Card – If you can’t qualify for a regular credit card due to bad credit, consider a secured credit card. They simply require a security deposit for approval, and payments are reported to the credit bureau(s).

Bottom Line

Your credit score range tells you — and your lenders — how you're likely to handle borrowed money. In Canada, aim for 660 or higher to be in "good" territory. Wherever you sit today, your score isn't fixed: with on-time payments and low balances, you can move up the range over time. Responsible use of your credit cards and loans, over time, may improve your credit score and therefore help you to qualify for other larger loans, for example, a mortgage, in the future.

Credit Score Range FAQs

Is 700 a good credit score in Canada?

What is a good credit score in Canada?

What is a bad credit score in Canada?

What is the average credit score in Canada?

Can I get a free credit score in Canada?

What credit score do I need to get a mortgage in Canada?

References

- Borrowell. (2026). What is the average Canadian credit score? https://borrowell.com/blog/highest-canadian-credit-score-study

- Equifax Canada. (n.d.). What is a good credit score? https://www.consumer.equifax.ca/personal/education/credit-score/