When you’re looking to borrow money, it can be tough to choose between a personal loan and a line of credit. Along with other personal loan alternatives, understanding how personal loans and lines of credit differ in structure, flexibility, and cost can help you choose the borrowing solution that best fits your plans.

Key Points:

- Personal loans provide a lump sum with fixed payments, while lines of credit offer flexible, ongoing access to funds.

- Lines of credit typically have variable interest rates and only charge interest on what you use, whereas personal loans may have fixed or variable rates on the full amount.

- Personal loans are better for one-time expenses with predictable repayment, while lines of credit suit ongoing or unpredictable costs.

- Choosing between the two depends on your needs, cash flow flexibility vs. payment stability, and overall financial situation.

Personal Loan Vs. Line Of Credit Overview

There are several differences between personal loans and personal lines of credit:

| Personal Loan | Line Of Credit | |

| Disbursement Method | Lump sum payment | Reusable; any portion can be accessed at any time |

| Secured Or Unsecured | May be either secured or unsecured | May be either secured or unsecured |

| Interest Rate | Fixed or variable | Variable |

| Loan Amount | Varies by lender (average amounts vary between $500 – $35,000+) | Varies |

| Repayment | Installment payment schedule | – Pay interest only on the amount you use during the draw period. – Interest and principal must be repaid by end of the repayment term. |

What Is A Personal Loan?

A personal loan involves borrowing a certain amount of money from a bank or alternative lender. In return for borrowing the funds, the borrower agrees to repay the loan in installments.

Each payment includes both the principal amount as well as the interest portion. The amount of money that goes towards interest will depend on the interest rate and the loan term.

Personal loans are typically unsecured, which means there is no collateral used to back up the loan. Unsecured loans tend to be riskier for lenders, and as such, they usually come with higher interest rates compared to secured loans.

Personal Loan Features

- Fixed Loan Amount: You receive the full loan upfront as a lump sum.

- Set Repayment Schedule: Payments are made over a set period, typically from 1 to 7 years.

- Fixed Payments: Payments are made in fixed installments, usually monthly

- Fixed Or Variable Interest Rate: Many personal loans use fixed rates, but some lenders offer variable options.

- No Collateral Required: Personal loans are typically unsecured, meaning you don’t need to pledge assets. That said, some lenders may allow collateral to reduce risk and improve the borrower’s chances of loan approval.

- Used For Many Purposes: Common for debt consolidation, home projects, medical expenses, or major purchases.

How Much Can You Borrow With A Personal Loan?

The amount of money that you are able to borrow will depend largely on your credit score, payment history, income, and debt load. In general, lenders offer personal loans between $500 to $35,000+, though some lenders may offer higher amounts.

Borrow Up To $50,000

What Interest Rate Will You Be Charged?

The interest rate you are charged will also depend on your financial and credit profile. The lower your credit score and the higher your debt-to-income ratio, the higher you can expect your interest rate to be.

It’s best to check your credit score by pulling your credit report before applying for a personal loan. This will help you get a better idea of how easy or difficult it may be to get approved for a personal loan, as well as what type of interest rate you can expect.

You can check your credit score for free using Loans Canada’s CompareHub tool.

Can You Use A Personal Loan To Pay Off Your Credit Card Debt?

Yes, you can use a personal loan to pay off your high-interest credit card debt. Given how high credit card rates tend to be on outstanding balances, it might make financial sense to take out a lower-rate personal loan to get rid of that high-interest credit card debt.

Not only can this save you money over time, but it can also make monthly payments more affordable.

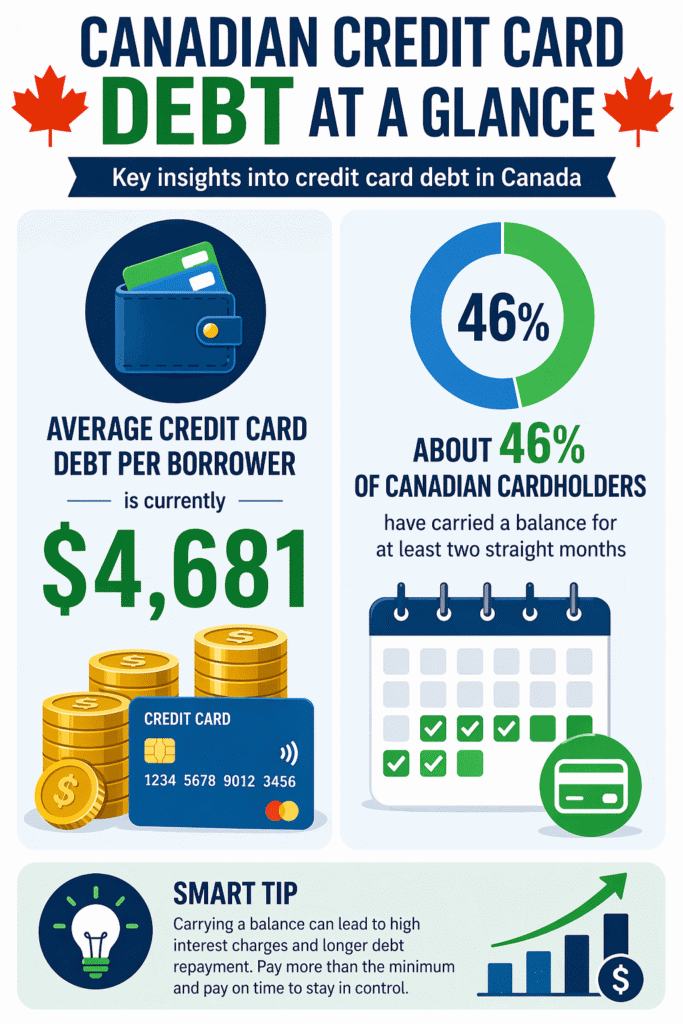

How Much Credit Card Debt Do Canadians Carry?

Can You Use A Personal Loan As A Debt Consolidation Solution?

Yes, you can consolidate your debt using the funds from a personal loan.

Debt consolidation involves taking out a new, larger loan to pay off several smaller loans, usually at a much lower interest rate. Rather than paying a number of debts at varying times of the month and at different interest rates, borrowers can use the money from a personal loan to replace all that, making it much easier to manage.

That said, it only makes sense to take out a personal loan to consolidate debt if the interest rate is much lower than all current loans.

Pros And Cons Of Personal Loans

Personal loans come with their own set of advantages and drawbacks, and understanding both can help you decide whether this type of borrowing fits your financial needs.

Pros:

- Predictable Payments: Fixed monthly payments make budgeting straightforward.

- Fixed Interest Rates: Fixed rates protect you from rising borrowing costs.

- Great For Bigger Expenses: Ideal for large, one‑time needs like renovations or debt consolidation.

Cons:

- Limited Flexibility: Once the funds are issued, you can’t adjust the loan amount.

- Interest On Full Amount: You pay interest on the entire loan even if you don’t use all the money.

- Possible Early Prepayment Fees: Some lenders charge penalties if you pay off the loan early.

What Is A Line Of Credit?

A line of credit involves borrowing a certain amount of money from a creditor. Unlike a personal loan, the funds with a line of credit do not have to be withdrawn in one lump sum.

Borrowers can take out as much or as little money as needed up to the specified credit limit. Only the money withdrawn is charged interest rather than the entire credit limit. Once that money is repaid, no further interest will be charged until the next withdrawal.

Line Of Credit Features

- Flexible Borrowing: Access funds as needed rather than receiving a lump sum.

- Revolving Credit: As you repay, your available credit becomes available again.

- Variable Interest Rates: Line of credit interest rates typically fluctuate with the market.

- Pay Interest Only On What You Use: You’re charged interest only on the amount you’ve borrowed, not the entire credit limit.

- Useful For Ongoing Or Unpredictable Expenses: Ideal for home projects, emergencies, or cash‑flow gaps.

How Do You Repay A Personal Line Of Credit?

A personal line of credit differs from a traditional loan in many ways, including how you repay what you borrow.

With a personal loan, you would be required to make regular payments on pre-scheduled dates until the full loan is paid back by its due date. But with a personal line of credit, the repayments are more flexible.

The following are the more common types of repayments on a personal line of credit:

Draw And Repayment Periods

When you apply for a line of credit, you’ll be given a specific period within which you can withdraw money, which is referred to as the “draw period.” During this time, you’re only obligated to pay the interest portion of your payments. If you carry an outstanding balance by the time the draw period ends, you’ll enter a repayment period.

During this period, you cannot make any more withdrawals and you’ll have to make monthly installments to repay any remaining balance. The specific terms of repayment may vary by lender.

Balloon Payments

With this type of repayment arrangement, the full balance must be repaid at the end of the draw period.

Demand Line Of Credit

A less common way to repay a line of credit is through a demand line of credit. With this repayment plan, the lender has the right to require full repayment at any time.

Pros And Cons Of A Line Of Credit

A line of credit comes with its own mix of advantages and drawbacks, and knowing both can help you decide if this flexible borrowing option fits your financial situation.

Pros:

- Flexible Access: You can borrow funds whenever you need them.

- Interest On Withdrawn Funds Only: You’re only charged interest on the amount you actually borrow.

- Revolving Credit: As you repay, your available credit replenishes for future use.

Cons:

- Variable Rates: Fluctuating interest rates can increase your borrowing costs.

- Flexible Repayment Structure: Minimal payment requirements can make it easier to stay in debt longer.

- Risk Of Overspending: Ongoing access to funds can tempt you to borrow more than necessary.

Key Factors Lenders Consider Before Approval

Before approving either a personal loan or line of credit, lenders evaluate several financial factors, including the following:

- Credit Score: Higher scores typically qualify for better rates.

- Income Stability: Consistent income improves approval chances.

- Debt-to-Income Ratio: Lower ratios indicate better financial health.

Understanding these factors can help you improve your approval odds and secure better terms.

Where Can You Get A Personal Loan Or A Line Of Credit?

You can apply for a personal line of credit or a personal loan from a variety of sources, including banks, credit unions, and alternative online lenders.

Banks

The lending criteria for a personal line of credit and personal loan at a bank may be more stringent compared to other lenders. Generally speaking, you’ll need good credit and sufficient income to get approved by a bank for a personal line of credit or personal loan.

Credit unions

You may be able to secure a lower interest rate on your line of credit or personal loan with a credit union compared to a bank, but you will need to apply to become a member before applying for the loan.

Alternative online lenders

If you don’t meet the criteria for loans with a bank or credit union, you may have better luck with an alternative lender. These lenders offer financial products like personal lines of credit and personal loans to all sorts of borrowers, including those with bad credit. However, you will likely be charged a higher interest rate.

How To Apply For A Personal Loan Or Line Of Credit

To apply for a personal loan or line of credit, follow these steps:

Step 1: Check Your Credit Score

Review your credit score and credit report so you know where you stand before applying. Lenders use your score to determine your eligibility and interest rate.

That said, some alternative lenders may not conduct a credit check or require a good credit score. If you have bad credit, an alternative lender may be the way to go.

Step 2: Determine What You Need

Decide how much funding you require for your specific situation. Then, determine whether you need a one‑time lump sum of money (personal loan) or flexible, ongoing access to funds (line of credit).

Step 3: Compare Lenders

Look at banks, credit unions, and online lenders. Compare interest rates, fees, repayment terms, and borrowing limits to see where you can get the best deal.

Step 4: Gather Your Documents

Most lenders will ask for the following:

- Proof of income

- Employment details

- Identification

- Information about your debts and expenses

Make sure to have these handy when you apply

Step 5: Submit Your Application

Apply online, in person, or over the phone. You’ll provide personal information, financial details, and the amount you want to borrow.

Step 6: Wait For Approval & Review The Offer

Lenders review your credit, income, and overall financial profile. Approval can be instant or take a few days depending on the lender. Once you agree to the lender’s offer, you’ll sign the loan or credit agreement.

Step 7: Access Your Funds

Depending on the financing option you applied for, you’ll have access to the funds differently:

- Personal loan: You receive the full amount upfront.

- Line of credit: You can draw money as needed up to your approved limit.

Should You Use A Personal Loan Or Line Of Credit?

Both a personal loan and a line of credit can provide you with access to the money needed to cover a variety of expenses. But which one is best for you?

| When A Personal Loan Makes More Sense | When A Line of Credit Is The Better Choice |

| You need a one‑time lump sum | Your costs are spread out or unpredictable |

| You want predictable payments | You want flexibility |

| You’re trying to avoid ongoing debt | You want reusable access to funds |

Final Thoughts

A personal loan and a line of credit are great tools to take advantage of to gain access to much-needed cash. But the decision you make between one or the other will depend on your specific circumstances, namely your finances and what you need the money for.