Have you ever stopped to calculate how much of your income goes straight to monthly bills? You should, because your debt‑to‑income balance plays a major role in whether you can shop for a mortgage or even qualify for something like a $10,000 loan. Lenders rely on your debt service ratio to judge how comfortably you can handle new payments.

So what exactly is a debt service ratio, how do you calculate it, and how does your number hold up when it’s time to apply?

Key Points:

- You can get a $1,500 loan relatively easily, with approval often based more on income and repayment ability than perfect credit.

- Common options include personal loans, lines of credit, and payday loans, each with different costs, flexibility, and repayment structures.

- Payday loans offer fast access but come with very high fees and should only be used for urgent, short-term needs.

- Comparing lenders, understanding total costs, and having a clear repayment plan are key to avoiding unnecessary debt and financial strain.

Can You Get A Small $1,500 Loan?

Yes, you can get a $1,500 loan in Canada, and there are several lenders that specialize in quick, small loans.

Approval often depends more on your income and ability to repay than on having perfect credit. Because the loan amount is relatively small, many lenders offer fast applications, same‑day approvals, and funding in as little as a few hours. Just be sure to compare fees and terms so you choose the most affordable option for your situation.

| For context, smaller loan amounts, like a $100 loan or $500 loan, tend to have even faster approval times but may come with higher fees. |

Best $1,500 Loans

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Types Of $1,500 Loans

There are a handful of ways to get a $1,500 loan in Canada:

$1,500 Personal Loans

A personal loan allows you to borrow $1,500 in one lump sum, which you can use to cover your expenses and repay in installments. Loan conditions and requirements vary from lender to lender but applicants with stronger credit and incomes usually have less trouble qualifying and are able to secure better interest rates and terms.

Repayments are made via fixed installments over a set term. Generally speaking, $1,500 personal loans are unsecured, which means they’re not backed by collateral. That said, some lenders may allow you to secure the loan with a valuable asset, which could help to increase your odds of approval and secure a lower rate and better terms.

$1,500 Lines Of Credit

A $1,500 line of credit is a revolving form of borrowing that lets you access up to $1,500 whenever you need it, rather than taking the full amount upfront. You only pay interest on the portion you actually use, which can make it more affordable than a fixed loan.

As you repay what you’ve borrowed, your available credit replenishes, similar to a credit card. This flexibility makes it useful for covering small, recurring, or unexpected expenses without reapplying each time.

$1,500 Payday Loans

A $1,500 payday loan is a short‑term loan designed to give you quick access to cash, usually with repayment due on your next payday. These loans are known for fast approvals and minimal documentation, making them accessible even if you have bad credit.

In fact, payday loan amounts are typically capped at $1,500. So, if you wanted a $2,500 loan for instance, you’d need to seek one in the form of an installment loan or other traditional form of financing.

However, they typically come with much higher fees and interest costs than traditional loans. Plus, they must typically be repaid in one lump sum rather than spread out over installments.

Because of this, they’re best used only for urgent, unavoidable expenses when no lower‑cost options are available.

$1,500 Loan Types Overview

| Personal Loans | Lines Of Credit | Payday Loans | |

| What It Is | Borrow $1,500 upfront and repay in fixed installments | Access up to $1,500 as needed and repay only what you use | Borrow $1,500 and repay in full on your next payday |

| Cost | Moderate, predictable rates | Variable interest; interest only on used amount | Very high fees and costs |

| Repayment Term | Months to years | Ongoing, revolving credit | Typically 14-62 days |

| Credit Requirements | Fair to good credit | Flexible; depends on lender | Usually minimal credit checks |

| Best For | Planned expenses and structured repayment | Ongoing or unpredictable expenses | Emergencies when no other options exist |

How To Get A $1,500 Loan

To get a $1,500 loan in Canada, follow these steps:

Step 1: Shop Around

Compare loan rates and conditions from a variety of lenders. Many lenders offer pre-approvals so you can see how much you may qualify for and at what rates.

You can also use a loan comparison platform, like CompareHub, to compare lenders and their offers. When evaluating different lenders, also make sure your lender is a reputable business with good customer reviews.

Step 2: See If You’re Eligible

Once you have a few lenders in mind, find out their minimum eligibility requirements. This will ensure that you apply with lenders you know you have a chance of qualifying with.

Every lender has different prerequisites, but to become eligible for any loan in Canada, you’ll generally need to:

- Be a permanent resident or citizen

- Be at least the age of majority in your province or territory (18 – 19+)

- Have a regular income that would sufficiently cover your loan payments

- Have a bank account that’s been active for at least 3 months

Step 3: Apply

If you’re eligible to get a $1,500 loan, you can apply by going to your lender’s website or service location to submit your application. During this process, you may have to provide personal and financial information, like the following:

- Personal info (name, date of birth, permanent address, phone number)

- Email address

- Social Insurance Number (SIN)

- Government photo ID (passport, driver’s license, etc.)

- Proof of income/bank account (recent pay stub and bank statement)

- Proof of residency (recent utility bill or document with your address)

- Pre-authorized debit form or VOID cheque (for deposits and payments)

Step 4: Wait For A Reply

Once you’ve applied, most lenders will inform you whether you’ve been approved or rejected within 24-48 hours. Some will even contact you within a few minutes. If all goes well, you should receive your loan contract shortly after and your funds on the same day or the next business day.

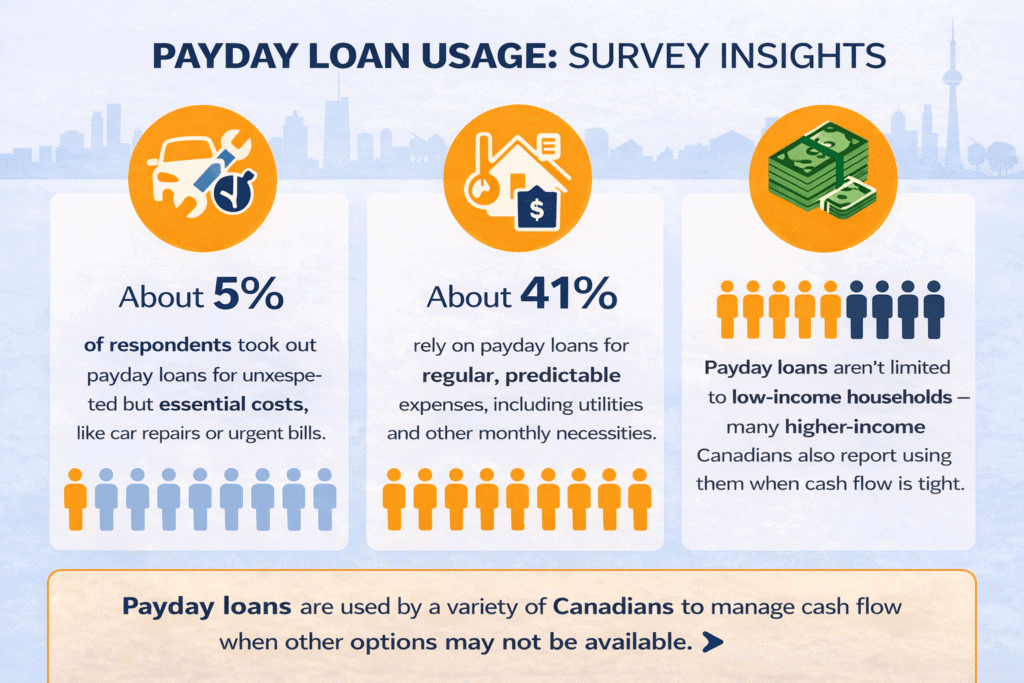

How Much Do Canadians Rely On Payday Loans?

How To Choose The Right Lender

Not all lenders offer the same experience, and choosing the right one can significantly impact both your costs and overall satisfaction.

When comparing lenders, consider the following:

- Interest rates and total borrowing cost

- Repayment flexibility (installments vs lump sum repayment)

- Speed of funding

- Transparency of terms and fees

- Customer reviews and reputation

Online lenders often provide faster approvals, while banks and credit unions may offer lower rates for qualified borrowers. Finding the right balance between speed and affordability is key.

Learn How To Qualify For Other Loan Amounts

How To Increase Your Chances Of Qualifying For A $1,500 Loan

As mentioned, every lender has different requirements for their loans, so there’s no real way to get guaranteed approval, but you can increase your approval chances by doing the following:

Improve Your Credit

If you have bad credit, take the time to improve it before you apply.

- Make On-Time Bill Payments: You can improve your credit score by making all your payments on time, since payment history is the biggest factor lenders look at.

- Reduce Your Credit Utilization: Keeping your credit balances low (ideally under 30% of your limit) also helps boost your score over time.

- Fix Errors On Your Credit Report: Finally, check your credit report regularly to catch errors or outdated information that could be dragging your score down.

| Pro Tip: Check your credit score for free before applying for a loan by using Loans Canada’s CompareHub tool online. |

Earn More Income

While $1,500 is a relatively small loan these days, most lenders have a minimum monthly income requirement that you must pass to be approved. If you’re not employed or you’re living off other forms of income, like government benefits, you may have to apply with an alternative/private lender.

Don’t Apply Too Often

When you apply for credit, a hard inquiry will be conducted, which can lower your credit score by a few points. Not only can this harm your credit as a whole, but lenders may also see all the recent applications in your credit history and turn you down, especially if you were denied a lot in the past.

Cost Of A $1,500 Personal Loan

Personal loans are installment-based loans with requirements, conditions and interest rates that vary according to the lender, as well as the applicant’s financial aptitude.

Here’s a basic example to show you what a $1,500 personal loan could cost in Canada:

| Personal Loan Amount | $1,500 |

| Payment Term | 6 months |

| Interest Rate | 24.99% APR |

| Monthly Payment | $268.53 |

| Total Interest | $111.21 |

| Total Cost | $1,611.21 |

Cost Of A $1,500 Line Of Credit

The cost of your line of credit depends on how much of the credit account you access, how often you access it, and the interest rate you’re charged on the withdrawn amount.

For illustration purposes, the following chart outlines how much your $1,500 line of credit could cost you based on a rate of 15% and a full repayment within 30 days:

| Amount Borrowed | $1,500 |

| Interest Rate | 15% |

| Cost For 30 Days | $18.75 |

| Total Cost | $1,518.75 |

Cost Of A $1,500 Payday Loan

Most payday loans have 14-day terms (the average length of time between paycheques), along with very high-interest rates and fees. Maximum rates depend on the provincial laws of your region.

Here’s what a Canadian payday loan can cost you:

| Province/Territory | Loan Amount | Interest/Fee | Cost | Total Cost |

| All Provinces Except Quebec | $1,500 | $14/$100 borrowed | $210 | $1,710 |

| Quebec & All 3 Territories | $1,500 | 35% APR | ~$20.14 | ~$1,520 |

Other Ways To Get $1,500 Loan

If a traditional loan isn’t the right fit, there are several other practical ways to access $1,500, depending on your financial situation and how quickly you need the funds.

- Use A Credit Card: If you have a credit card, using it for the expense can be cheaper than high‑cost loans, especially if you can pay it off quickly or use a low‑interest promotional period.

- Use A Credit Card Cash Advance: Again, having a credit card can allow you access to funds needed to cover a small expense. With a credit card cash advance, you can access the funds from your account immediately. Just keep in mind that interest will start to accrue right away, and cash advance rates are usually a bit higher than purchase rates.

- Inquire About A Pay Advance From Your Employer: Some workplaces offer small advances or programs that let you tap into money you’ve already earned earlier than your payday.

- Look Into Payment Plans: If you’re looking to cover the cost of a product or service, inquire about whether the retailer offers a Buy Now Pay Later (BNPL) service. This allows you to spread the cost of a purchase over smaller installments over a period of time without the need to spend time applying for a separate loan and waiting for approval and funding.

Risks To Be Aware Of Before Borrowing

While a $1,500 loan can be helpful, it’s important to understand the potential risks before committing:

- High Costs For Short-Term Loans: Payday loans, in particular, can be significantly more expensive than other options

- Debt Cycle Risk: Repeated borrowing to cover previous loans can quickly escalate financial strain

- Impact On Credit: Missed or late payments can negatively affect your credit score

- Fees & Penalties: Late fees or NSF charges can increase your total repayment cost

| A good rule of thumb is to ensure you have a clear repayment plan before accepting any loan offer. |

When Does A $1,500 Loan Make Sense?

A $1,500 loan can be a practical solution when used for necessary, urgent expenses instead of leisurely spending. Understanding when it makes sense to borrow can help you avoid unnecessary debt.

Situations where a $1,500 loan may be appropriate include the following:

- Emergency expenses (car repairs, medical bills, urgent home repairs)

- Short-term cash flow gaps between pay periods

- Consolidating small, high-interest debts into one manageable payment

On the other hand, using a loan for non-essential purchases or ongoing financial shortfalls can lead to a cycle of debt. In these cases, it may be better to explore budgeting adjustments or lower-cost borrowing options.

Final Thoughts

Getting a $1,500 loan in Canada is usually straightforward once you understand your options and what lenders look for. Whether you choose a personal loan, line of credit, payday loan, or another alternative, comparing rates and fees can help you avoid unnecessary costs. With a clear plan and the right lender, you can access the funds you need while keeping your financial health on track.