As helpful and convenient as some credit products are, they can make it easy to rack up debt. This is particularly problematic with high-interest credit products such as credit cards and even some of the best personal loans. When coupled with your other daily expenses, these debts can be difficult to pay down. When that happens, it can be tempting to make a partial payment just to avoid penalties.

However, there are consequences that may occur if you don’t pay your bills in full. Keep reading to find out what happens if you make partial payments.

Key Points:

- Partial payments may prevent immediate loan default, but they often lead to additional interest and potential penalties.

- Many lenders still consider partial payments as “late” on fixed loans.

- Repeated partial payments can negatively impact your credit score and long-term financial health.

- Communication with lenders can often mean better alternatives like deferrals or hardship programs.

Partial Payments Vs. Late Payments

In Canada, it can be tough to find a credit product that doesn’t result in some kind of penalty when you don’t pay your debts in full and on time. That said, there are a couple of key differences between making partial payments and late payments:

What Is A Partial Payment?

As the name suggests, a partial payment is when you don’t pay a bill off completely. Instead, your lender may allow you to make part of your payment, provided you agree to pay the rest of your debt off at a later date.

These payments are commonly seen with revolving credit products, like credit cards and lines of credit. However, it can be an option with other types of debt.

What Is A Late Payment?

Unlike partial payments, most lenders aren’t as forgiving when you don’t pay your debts on time. Even if you pay a day or two later, you could be charged a penalty, as well as extra interest.

While some credit products have grace periods, payments after it can have serious consequences. Late payments can result in more serious financial consequences than partial payments.

How Lenders Treat Partial Payments

Not all lenders treat partial payments the same way, especially when it comes to the type of credit product involved.

| Installment Loans | Revolving Credit |

| For installment loans, like mortgages, car loans, and personal loans, lenders typically don’t accept partial payments, and often hold them in account until the full payment is made. This means the following may apply: – Your payment may not be officially credited – You could still be reported as late – Interest continues to accrue on the unpaid balance | For revolving credit, like credit cards, partial payments are more flexible, as long as you meet the minimum payment amount. However, this means more interest charged overall. |

Understanding how your specific lender applies payments is important before deciding to make a payment that’s less than the full amount.

Consequences Of Making A Partial Payment On A Loan

Debt doesn’t just apply to credit products. Plenty of financial products and services can involve payments. For example, utility providers set their own penalties for customers that don’t pay as agreed.

Here are some other common products that could have various consequences when you make partial payments:

Consequences Of Making A Partial Payment On A Mortgage

Your mortgage is one scenario where it’s a really bad idea to stray from your agreement. Although some lenders will tolerate it under exceptional circumstances, most will apply a hefty penalty to your final loan balance. Generally, the amount you have to pay is based on how many days late or how short the payment is.

Additionally, falling behind on payments can increase the risk of loan default, which may trigger more serious actions from your lender if the issue isn’t resolved quickly.

These consequences could happen if you cannot make a full mortgage payment:

- Late Fees: Most lenders will consider a partial payment “late”, even if it’s only a few dollars short. Afterward, they may charge you a penalty fee and extra interest. These fees can quickly add up and significantly increase your total mortgage balance.

- Less Creditworthiness: Next, most lenders will report your late payments to Canada’s credit bureaus, which can decrease your credit score. They will also appear on your credit report for several years. Moreover, they can be seen by lenders, who may not approve you for new credit products or good interest rates. If you’ve made partial payments, it’s best to check and track your credit score.

- Loss of Asset/Foreclosure: Since mortgages are large, risky loans, they’re normally secured against your property. If you can’t justify your late payments, many lenders will consider foreclosing your home or seizing your asset after 90 – 120 days.

Consequences Of Making A Partial Payment On A Credit Card

Credit cards are one of the few products that allow partial payments without penalty, provided you pay at least the minimum amount on your monthly balance statements. However, there are consequences for paying under the minimum or making too many partial payments, such as:

- Late Fees & Interest: Like most credit products, failing to cover your minimum monthly credit card balance can lead to a penalty fee and additional interest. Although credit card late fees may not be too steep, the interest that’s applied to your unpaid balances can get very expensive, very quick.

- Faster Decline In Creditworthiness: If your lender reports to Equifax and/or TransUnion, any late payments will end up on your credit report for multiple years. Plus, carrying large amounts of unpaid debt on your card can gradually cause a decline in your credit score and make you less creditworthy.

- Account Charge-Off & Debt Collection: After 180 days of late payments, most lenders will deactivate your account and sell it to a collection agency. Not only could this leave you with a lack of credit, but the debt collection procedures can also be followed by lawsuits, wage garnishment and other legal consequences.

Consequences Of Making A Partial Payment On A Personal Loan

No matter the size of your personal loan, your lender can still subject you to some severe penalties when you don’t make full payments, like:

- Late Fees & Interest: Since most lenders don’t accept partial payments, some personal loans involve much higher late fees and interest rates for late payments than many credit cards do.

- Credit Damage: It can be hard to find a good lender that doesn’t report loan activity to at least one credit bureau. So, when you’re late on too many payments, your credit report, credit score, and creditworthiness can suffer greatly.

- Charge-Off & Collections: Your lender will decide when your personal loan account is charged off and sold to a collection agency. If you have a large loan debt, the agency could be even more inclined to take you to court.

Consequences Of Making A Partial Payment On A Car Loan

Any type of vehicle loan can also involve a lot of risk for the lender and some major consequences can apply when you try to make a partial payment, like:

- Late Fees & Interest: Car loans are no exception to the late payment rule, whether you’re financing your vehicle through a bank, alternative lender or dealership. This is especially true for newer and more valuable models.

- Credit Damage: Many car loan providers also report to Equifax and/or TransUnion. So, if you don’t make full payments, you may see a big drop in your credit score, along with all the typical damage to your credit report.

- Collections & Repossession: Similar debt collection penalties can apply when you default on an auto loan. Plus, your loan may be secured against the car, so your lender will have the right to repossess it if you miss too many payments.

Consequences Of Making A Partial Payment On Tax Debt You Owe

Unlike the everyday credit product, your income tax debts are handled by the Canada Revenue Agency (CRA). As such, more serious legal and financial consequences can apply if you don’t make full, timely payments. This includes:

- Late Fees & Interest: When you don’t pay your taxes, the first thing the CRA will do is charge you a penalty. This fee usually amounts to 5% of your debt, plus an extra 1% of your balance owing for every month that passes without payment.

- Wage/Income Garnishment: If you fail to pay your income taxes without an explanation, the CRA will take legal action. This often results in them being able to periodically deduct a portion of your debt from your income or bank account.

- Loss Of Assets: If your tax debt is large enough and your income is insufficient, the CRA may collect payment by seizing and selling your assets. This can lead to the repossession of your car or, in the worst of cases, foreclosure of your home.

Thankfully, if you provide a viable explanation for why you can’t report your taxes on time and arrange to pay the rest of your debt off in installments, the CRA may allow you to make a partial payment. For this to work, you’ll have to prove that you already tried to cover your debt by borrowing money or decreasing your expenses.

Consequences Of Making A Partial Payment On Government Student Loan Debt

There are several credit products that you can qualify for as a student, such as a guaranteed loan from the federal or provincial/territorial government. Sadly, if you don’t pay as agreed, this kind of loan can also lead to severe drawbacks, such as:

- Penalties & Collections: It takes about 270 days of missed payments for the government to send your defaulted account to the CRA for debt collection1. Once that happens, they can withhold your tax refund and use it to repay your debt.

- Legal & Financial Actions: The CRA also has the ability to file a lawsuit against you, freeze your bank account and garnish your income until your full balance owing (plus interest and fees) is repaid.

- Reduced Creditworthiness: Like other credit products, government student loans generally get reported to Canada’s credit bureaus. So, if you have any unpaid debt, it can damage your credit history, rating, and score.

Although these consequences are serious, the government might be understanding if you have a valid reason for making a partial payment.

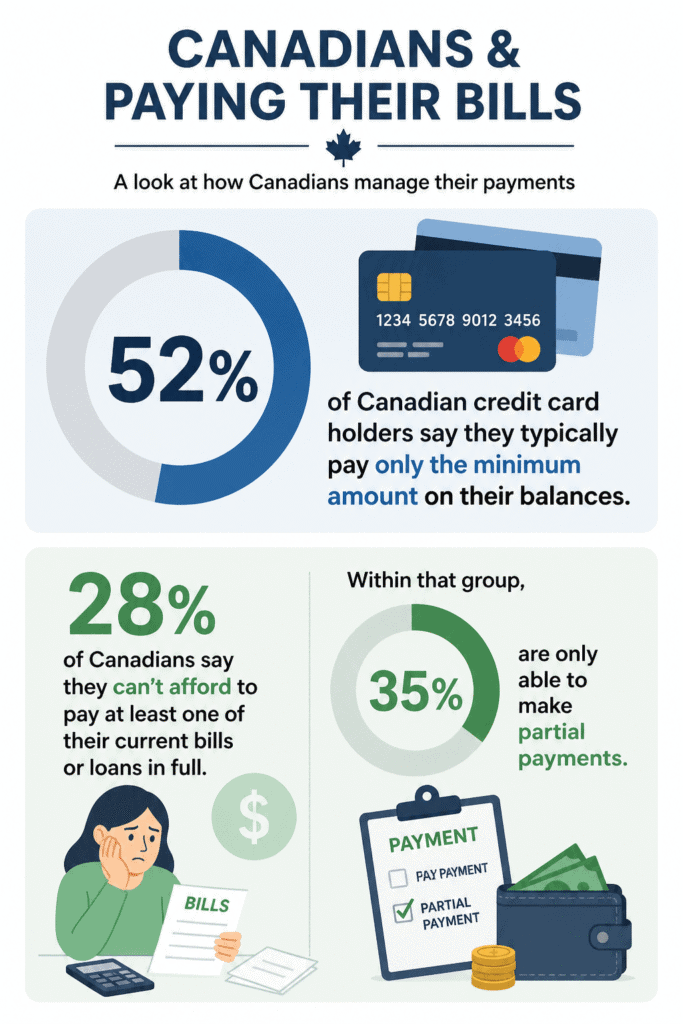

How Many Canadians Are Only Making Partial Payments?

What Happens To Interest When You Make Partial Payments?

One of the most overlooked consequences of partial payments is how interest continues to compound. When you don’t pay your full balance:

- Interest accrues on the remaining principal

- Future payments go more toward interest than principal

- Your total repayment cost increases over time

| For example, carrying a balance on a high-interest credit card can dramatically increase the cost of borrowing if only partial payments are made consistently. In fact, making only minimum or partial payments can extend repayment timelines by years. |

Impact On Your Credit Utilization Ratio

Partial payments can also damage your credit score through utilization.

Credit scoring models that credit bureaus use heavily weigh your credit utilization ratio, which is the percentage of available credit you’re using. If you consistently make partial payments, your balances remain high—pushing utilization up and lowering your score, even if you never miss a due date.

What Should You Do If You Can’t Make A Full Payment?

If you’re only able to make a partial payment this month, there are a few different options that can help you out of a jam, including the following:

Speak To Your Creditor/Institution

Reaching out to your creditor early can prevent your situation from escalating, especially if you don’t think you’ll be able to make upcoming payments.

Many lenders are more flexible than people expect, and they may offer temporary relief options such as deferred payments or adjusted schedules. Even if the solution isn’t perfect, communicating before you miss a payment can help you avoid late fees, protect your credit, and reduce stress.

Check If There’s A “Skip Payment” Option

Some lenders build skip‑payment features directly into their contracts, allowing you to pause one or more payments without penalty. This option is often available for auto loans, personal loans, and certain lines of credit, though eligibility may depend on your payment history.

While interest may still accrue, skipping a payment can give you short‑term breathing room when cash flow is tight.

Refinance

Refinancing involves replacing your current loan with a new one that has different terms, which can make repayment more manageable. Depending on your credit and the lender’s policies, you may secure a lower interest rate, extend your repayment period, or reduce your monthly installments.

This strategy is especially common with mortgages but can also apply to other loan types if the lender allows it.

Consider A Balance Transfer

A balance transfer lets you move debt from one credit product to another, often with lower interest or promotional rates. This can significantly reduce the cost of carrying a balance, particularly if you’re transferring from a high‑interest credit card.

It’s important to check for transfer fees and understand how long any promotional rate lasts to maximize the benefit.

Find A Credit Counsellor

A credit counsellor can assess your financial situation and recommend strategies based on your needs. They can help you explore structured solutions such as debt management programs, which consolidate payments and may reduce interest.

Look Into The Repayment Assistance Plan (RAP)

If your debt is tied to government student loans, you may qualify for the Repayment Assistance Plan, which adjusts your payments based on your income and family size. RAP can reduce or even temporarily eliminate required payments if your financial situation is strained.

Over time, the program may also cover a portion of your interest or principal, depending on your eligibility.

Speak With A Licensed Insolvency Trustee (LIT)

A Licensed Insolvency Trustee is legally authorized to administer debt relief programs, such as consumer proposals and bankruptcies. They can review your finances, explain each option, and help you determine whether insolvency is necessary or if alternatives exist.

When Partial Payments Might Make Sense

While generally not ideal, partial payments can be useful in specific situations:

- To avoid immediate default while negotiating a hardship plan

- To maintain a good working relationship with a lender during temporary financial issues

- When combined with an alternative payment arrangement or loan deferral agreement

| Warning: Making partial payments without a clear plan can worsen long-term financial outcomes. |

Final Thoughts

Before making a partial payment, make sure to find out about the potential consequences. They can do significant harm to your credit and finances when you’re not careful. After all, while a full payment might not seem affordable at first, the penalties and interest that gets added to your unpaid debt may not be worth the trouble.

FAQs

Do partial payments affect your credit score?

Can I pay off my debt using partial payments?

Is a partial payment considered a late payment?

Does making a partial payment help avoid late fees?

How long do partial or missed payments stay on your credit report?

References:

1National Student Loans Service Centre (NSLSC). Stages of a Student Loan. Canada.ca

2Government of Canada. How long information stays on your credit report. Canada.ca