The cost of buying and owning a home in Ontario goes far beyond the purchase price. From land transfer tax to insurance, utilities, and surprise maintenance costs, the real expenses can add up fast. And if you’re still figuring out how to shop for a mortgage, understanding these costs upfront can help you choose the right lender, the right rate, and the right budget before you start house‑hunting.

Key Points:

- The total cost of homeownership in Ontario can exceed $5,000 per month on average, including mortgage, utilities, insurance, and other expenses.

- Mortgage payments are the largest cost, but property taxes, maintenance, and condo fees add large ongoing expenses.

- Even a 1% increase in interest rates can raise monthly mortgage payments substantially and add tens of thousands in total interest.

- Buyers should also budget for hidden upfront and ongoing costs to stay financially stable.

What Is The Average Monthly Housing Cost In Ontario?

Given the average costs of various expenses listed below, the average homeowner in Ontario could spend over $5,000 a month. Keep in mind that these figures could be much different than your specific situation.

As a general rule, you shouldn’t spend more than 39% of your gross monthly income on housing costs. Keeping your expenses under this threshold will help you avoid becoming “house poor” and protect your financial health.

Monthly Costs Of Owning A House In Ontario

On top of the costs associated with buying a home, there are several ongoing expenses that you’ll need to cover as a homeowner in Ontario, including the following:

Mortgage Payments

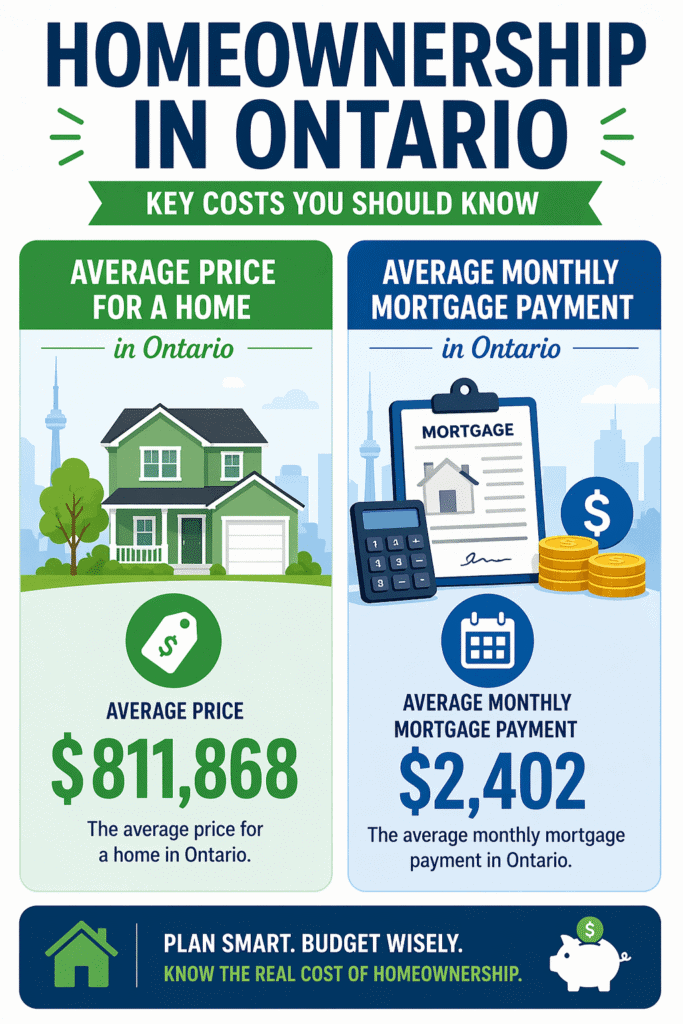

According to the Canada Mortgage and Housing Corporation (CMHC), the average monthly mortgage payment in Ontario is $2,4021.

Home Insurance

The average cost of home insurance in Ontario is anywhere from $1,200 to $1,700 per year, which comes to $100 to about $142 per month2. That said, the amount you pay can be much higher than this, depending on the following:

- Where your home is located

- The value and age of your home

- Your home’s contents

- Type of heating (ie. gas versus wood-burning fireplace)

- Your insurance claims history

- Your home’s proximity to a fire hydrant/fire hall

You’ll need to consult with an insurance broker to find out exactly how much you can expect to pay in home insurance.

Energy And Utility Bills

As a homeowner, you’ll have multiple utility and energy bills to pay including internet, cable, and home phone.

Other bills to consider are energy bills such as hydro electricity and gas. Home energy spending in Ontario varies across the province as a result of differences in:

- Energy sources used

- Household income

- Cost of energy distribution to the region

- Location

- Service provider

That said, the average household in Ontario spends roughly $2,128 per year on home energy, according to the Financial Accountability Office of Ontario, which works out to about $177 per month3. The amount of energy you use and the features of your home will ultimately determine how much you will pay per month in energy bills.

Water Bills

Average water bills in Ontario cost roughly $91.25 per month, which adds up to nearly $1,100 per year4. Homeowners may be able to save money on their water bills, however, thanks to the Ontario Trillium Benefit.

This tax-free benefit is meant to help alleviate the high costs of energy bills and certain taxes. Eligible low- to moderate-income residents of Ontario can receive up to $290 per month through the OTB, based on income and family status5.

For renters, the cost of water may or may not be included in the rent price, depending on the location. Renters typically pay for water if the place they’re renting is not a condo.

Water Heater Tank Rental

The price you pay for renting your hot water tank depends on a few things, like its capacity, type, brand, and energy efficiency level. That said, you can expect to pay anywhere from $16 to $60 per month6.

If you’re a homeowner, keep in mind that water heater rental companies may use tactics to convince you that renting your hot water tank is better than owning. This way, they can lure you into an ongoing contract that requires you to pay rent for the tank every month. You can be locked into these contracts for years and may be subject to regular increases in rental rates.

If you choose to rent your hot water tank, be sure to include this added cost to your monthly budget. But before you sign an agreement, make sure to weigh the costs of owning versus renting your water tank.

Condo Fees

If you’re part of a homeowners association (HOA) or condo association, you may have to pay a monthly fee to them. HOA fees are used to pay for services in the community such as lawn care, snow removal or repairs of common areas.

Condo fees in Ontario average $650 per month7. Some condos include utilities in the condo fees. Make sure you understand what your condo fees cover.

Other Costs Of Owning A House In Ontario

The recurring costs mentioned above are not the only expenses you would need to cover to operate and maintain a home in Ontario. Other costs that you need to budget for include the following:

Property Taxes

Each municipality in Ontario has a property tax rate, which is applied to the assessed value of your property. Depending on where your home’s location and its size, you could spend anywhere from under $2,000 to well over $10,000.

Maintenance Costs

It’s recommended that homeowners budget about 1% of their property value per year to cover maintenance and repair costs. If your home is valued at $750,000, consider setting aside around $7,500 per year to maintain and upkeep your home.

Keep in mind that some years may be more expensive than others if major repairs are required.

The following are the types of maintenance costs you’ll encounter:

- HVAC

- Plumbing

- Electrical

- Roofing

- Landscaping

- Foundation

- Gutters

- Paint

Renovations And Upgrades

While not necessary, you may consider updating your home to suit your tastes and changing styles. Renovating and upgrading your home is also a good idea to ensure you maintain its value.

There are several upgrades and renovation projects you may consider, including the following:

- Energy-efficient upgrades

- Appliance upgrades

- Room or floor additions

- Basement finishing

- Paint job

- New deck or patio

- Garage remodelling

- Upgraded lighting

- Crown molding

- Floor refinishing

This list is by no means exhaustive, and the costs can range substantially. Depending on the type of project and its scope, you could spend a few thousand or even tens of thousands of dollars (or more) to complete any of these projects.

Before you renovate your home, consider the return on investment. In other words, make sure the cost is worth the value it adds to your home. Some projects bring in a higher ROI than others. Make sure you’re not spending more than what you may be able to recoup if you sell at some point.

What’s The Average Price Of A Home In Ontario?

According to the Canadian Real Estate Association (CREA), the average price for a home in Ontario is $811,8688.

The cost may be much higher or lower depending on the exact city and type of dwelling.

For example, a home in the Greater Toronto Area (GTA) can cost you $941,800 on average, while a home in Windsor can cost you an average of $574,900.

Do You Pay HST On A House?

In Ontario, HST is only charged on homes sold by builders. So, new homes are charged HST on top of the purchase price, though builders typically roll that fee into the purchase price. Existing homes are not typically charged HST because the owner is not a builder.

The total HST in Ontario is 13%, which is made up of 8% PST and 5% GST. For example, a new home that costs $800,000 would be charged $104,000 in HST.

Fortunately, eligible Ontario home buyers may qualify for the HST New Housing Rebate to recoup the cost of HST paid on a new home purchase. The most you may get back if you’re eligible for this rebate is $24,0009.

| Major Changes Coming To The HST New Housing Rebate In 2026 The Ontario HST New Housing Rebate is set for major changes in 2026. Under the 2026 Ontario Budget, a temporary enhanced rebate will eliminate the full 13% HST on eligible new homes priced up to $1 million, providing buyers with up to $130,000 back10. This enhanced rebate will apply to purchase agreements signed between April 1, 2026 and March 31, 2027. |

How Rising Interest Rates Impact Monthly Costs

Mortgage rates have a direct impact on affordability and monthly payments. Even a 1% rate increase can significantly raise your monthly payments.

To illustrate how much even the slightest rate difference makes on your mortgage costs, let’s compare two different rates on the same mortgage:

- Loan Amount : $500,000

- Loan Term: 5 years

- Amortization: 25 years

| 5% Interest Rate | 6% Interest Rate | |

| Mortgage Payment | $2,908.02 | $3,199.03 |

| Total Interest Cost | $372,407.48 | $459,709.94 |

| Total Loan Cost | $872,407.48 | $959,709.94 |

As you can see, even a 1% rate increase can cause your monthly payments to rise by $291. What’s more alarming is that you’ll spend $87,302.

Hidden Costs First-Time Buyers Often Miss

Many buyers focus on the down payment and mortgage, but overlook several “hidden” costs, including the following:

- Moving expenses (truck rental, storage, movers)

- Initial furnishing and appliances

- Immediate repairs after closing

- Utility setup fees and deposits

These one-time costs can easily add thousands to your upfront expenses.

Learn more: The Hidden Costs Of Buying A House In Canada

How Much Income Do You Need To Afford A Home In Ontario?

Understanding affordability is just as important as knowing the costs. Lenders in Canada typically use two key ratios to determine how much you can afford in a home purchase:

- Gross Debt Service (GDS): GDS measures how much of your gross (before‑tax) income goes toward housing costs, and should not exceed 39% of gross income.

- Total Debt Service (TDS): TDS looks at all your monthly debt obligations, not just housing. This includes your mortgage, credit cards, car loans, student loans, and any other debt payments. Your TDS should not exceed 44% of gross income.

Bottom Line

These expenses might seem daunting, but they’re the normal set of expenses that come with homeownership and illustrate why budgeting is so important. Familiarize yourself with these costs so you can ensure that the home you buy is affordable for you.

FAQs

What is the biggest cost after buying a house?

How much tax do you pay when you buy a house in Canada?

How much are closing costs?

How much is a home purchase in Ontario?

References:

1Canada Mortgage and Housing Corporation (CMHC). Average Scheduled Monthly Payments for New Mortgage Loans. cmhc-schl.gc.ca

2insurely. Average Home Insurance Cost Ontario. insurely.ca

3Financial Accountability Office of Ontario. Home Energy Spending in Ontario. fao-on.org

4ZenMove. Ontario Utility Bills: What to Expect for Electricity, Water, Gas & Internet Costs in 2026. ZenMove.ca

5Government of Ontario. Ontario Trillium Benefit. Ontario.ca

6Home Depot. Best Water Heaters for Your Home. HomeDepot.ca

7View Homes. Condo Fees Statistics (2026). ViewHomes.ca

8Canadian Real Estate Association. Ontario Real Estate Association. CreaStats.ca

9Government of Canada. GST/HST new housing rebate. Canada.ca

10Government of Ontario. Ontario Expanding HST Rebate to Lower the Cost of New Homes in Partnership with the Federal Government. Ontario.ca

[/faq]