Filters

Loading...

Unfortunately we couldn't find you a provider with the given filters

The capital of Manitoba, Winnipeg is the largest city in the province, home to just over 705,000 people. Located at the bottom of the Red River Valley, the city is often referred to as “The Gateway to the West” because it’s an epicentre for railways and transportation. It’s also named after Lake Winnipeg, the 11th largest freshwater lake in the world. In 1914, a female black bear was purchased in Ontario by Lieutenant Harry Colebourn, who named her “Winnipeg”, after his hometown. The bear would later become the inspiration for A.A. Milne’s fictional character, Winnie-the-Pooh, spawning a series of children’s books in the late 1920’s, and is a franchise that still exists today.

Read this for a bit more information on loans, credit, mortgages, and financing in Winnipeg.

Although 25 years is the most common amortization period chosen by borrowers in Winnipeg, there are longer and shorter time frames to choose from. The one you decide will depend on a number of factors.

Shorter amortization periods are obviously appealing because they allow borrowers in Winnipeg to pay off their mortgages sooner rather than later. They’re also attractive because the overall amount of interest paid is much less than with longer amortization periods. The longer the payment period, the more interest you’ll have to pay, and vice versa.

Look at this to know if the interest on your mortgage is tax deductible in Canada.

But shorter amortization periods also mean that your monthly payments will be higher. If you’re able to make bigger payments comfortably, a shorter amortization period might be best. But if you struggle to make a certain amount of money each month, you may be better of with a longer amortization, which comes with lower monthly payment amounts.

Short amortization periods may also prove to be difficult for those who are self-employed or have an irregular income as a result of commission-based employment. They may also be tough for those who are buying a rather expensive home which would require a huge loan amount. In these cases, a short amortization period could tie up cash flow and might not be ideal.

Need to get out of debt fast with a low income? Try this.

The majority of people in Winnipeg and Canada, in general, usually go with a longer amortization period for the simple fact that their monthly mortgage payments will be lower. For many, the ability to afford a home purchase depends squarely on their ability to make their monthly payments. However, it should be noted that longer amortization periods mean the mortgage will take longer to pay off, and the overall interest amount paid will be much higher

True, the process of applying for a loan can be a bit confusing for some in Winnipeg, especially when there are so many misconceptions about loans themselves. Through word of mouth alone, certain facts about loans can naturally become skewed. These are just some of the myths that you might hear when you’re thinking about applying for a loan in Winnipeg:

Not all lenders in Winnipeg will check your credit score before approving you. However, they will look at your finances. Having too much other debt on your plate or showing any other signs of financial irresponsibility could lead to your application being rejected, especially if your lender considers you a bankruptcy risk. That’s why it’s best to prepare yourself and get your finances in order before you apply. Here are some steps that you can take to help you get approved:

While some lenders in Winnipeg do not check your credit score before approving you, it’s important to know that your score will be affected by a loan in various ways. For example:

Remember, a loan, especially when it’s being paid in a responsible manner is a valuable tool for building solid credit. That’s why it’s extremely important to make sure you select a lender in Winnipeg that will report your loan payments to one of the major Canadian credit bureaus, Equifax or TransUnion.

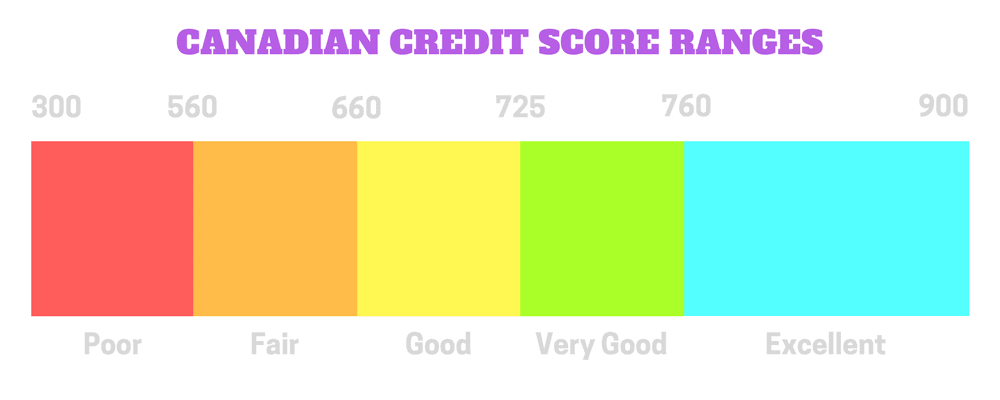

Do you know what your credit score range means? Check out this article.

Do you know what your credit score range means? Check out this article.

Does my credit score need to be high before I get approved for a loan? It depends on your lender. Some lenders in Winnipeg, like banks, will almost always check your credit score before approving you. However, certain lenders will not.

Will taking out a loan affect my credit score? Yes! As we mentioned above, if you take out a loan, but fail to make your regular payments on time, your credit score will be affected negatively. However, if your payments are on time and in full, your credit score will rise.

How can I increase my chances of getting approved? There are various ways to better your chances of getting the loan you need. Before you apply:

Is it possible to make my payments early? That usually depends on the lender. Most lenders in Winnipeg don’t allow advanced payments because they won’t be making as much in interest. If they do allow advanced payments, there might still be some restrictions. Wondering how lenders set their interest rates and if you can beat them somehow? Look here to know more.

Once my loan is approved, how long will it take to arrive? This also depends on your lender. Providing them with all the necessary information and filling out your application forms properly will make the process more efficient.

Is it better to use a credit card or a loan to pay my expenses? It depends on how expensive the purchase is. For smaller items such as food, clothes and other consumer goods (things that are easily paid off on a monthly basis) it can be more efficient to use a credit card. However, to finance something more expensive, it’s probably a better idea to use a loan.

One lender asked me for a deposit before I applied. Why? A legitimate lender is not supposed to charge you any money before you’re approved for your loan. If they demand a deposit upfront, do not pay them anything, they are likely scammers. Do not provide them with any of your personal information and stop all contact with them.

My bank keeps rejecting my applications. Why? All banks have specific policies when it comes to which clients can borrow from them. So, if you don’t have good credit, or don’t match their criteria in other ways, your application might be refused. However, banks are not the only lenders you can borrow from.

Can I apply for a loan if I do not have a credit history to show? Don’t worry. If you don’t have a credit history, it just means you’ve never made use of any credit products (credit cards, etc.). As long as they know you’ll be able to make your payments on schedule, most lenders will still approve you. However, when it comes to larger loans, like mortgages, having a healthy credit history and a record of financial responsibility is a good asset.

If you’re living in Winnipeg and you’d like some proper financing, look no further than Loans Canada.

As a senior, getting a loan can be more difficult due to lower income and age restrictions. Thankfully, there are many home equity loans for seniors i...

To better protect vulnerable borrowers, provinces have enacted legislation that sets boundaries on what alternative lenders can and can’t do.

Do you find yourself saying "I need my money today" often? Here are some simple and quick ways to get money quickly.

These are the best bad credit loan options in Canada right now. An easy list to make an easy choice. Here is everything you need to know!

A line of credit is a less rigid credit option. You only pay interest on what you use. That means flexibility. Read this article to get the

If you've been rejected a loan from easyfinancial, you'll be happy to know that there are plenty of easyfinancial loan alternatives in Canada.

If you are looking for loans like Fairstone, you can find them on Loans Canada. These Alternative lenders offer secured and unsecured loans.

easyfinancial vs. Fairstone? What is the difference? If you have bad credit, you can get a loan from this one faster

Maligayang pagdating sa Canada! Welcome to Canada! Do you know what is a soso (paluwagan)? Are they better than personal loans?

Did you get the CEBA loan? The CEBA loan repayment due date is close. Find out when and what can you do avoid default.

Get expert tips and guidance from a community of renown personal finance experts right here at Loans Canada. We're here to help you stay informed so you can make the best financial decisions.