Get a free, no obligation personal loan quote with rates as low as 6.99%

Get Started You can apply with no effect to your credit score

- What Your Credit Score Range Really Means

- Apple Card In Canada 2024

- The New Hudson’s Bay Mastercard Powered By Neo

- How To Get A Negative Item Removed From Your Credit Report

- Buying A House In Canada With Bad Credit In 2024

- Having Your Credit Checked For a Job in Canada

- Which Credit Bureau Do Lenders Check in Canada?

- Average Credit Scores By Province

- What Is The Average Credit Score In Canada By Age?

- How To Increase Your Credit Scores Immediately

- Can A Landlord Check Your Credit In Canada?

- Nyble vs. Bree: Which One Is Better?

- Neo Credit | Neo Financial Credit Card Review

- Canadian Tire Triangle Mastercard Review 2024

- Is The Vanilla Prepaid Card The Best On The Market?

- The Fidem Mastercard® Card Review

- Lendle Secured Mastercard Review

- Joker Prepaid Mastercard Review

- Canadian Tire World Elite Mastercard Review

- Fido Mastercard Review

- KOHO Credit Building Review 2024

- Scotiabank Momentum Visa Infinite Review

- Scotiabank Passport Visa Infinite Card Review

📅 Last Updated: October 4, 2021 ✏️ Written By Bryan Daly 🕵️ Fact-Checked by Caitlin Wood

Check out this infographic to learn all about the effect of bad credit on your life.

Check out this infographic to learn all about the effect of bad credit on your life.

Table of Contents show

Having bad credit is nothing to be ashamed of. Nevertheless, it can have a significant negative effect on your financial future, so it’s better to improve your credit however you can before you apply for a loan or other type of credit product in Regina.

If you’re looking for credit improvement in Regina Saskatchewan, we have all the information you need.

Do you live in another part of Saskatchewan? Do you need help improving your credit? Click here.

How and Why Lenders Check Your Credit

Whenever you apply for a credit product of any kind, the potential lender will have the ability to check your credit through one of Canada’s two main credit bureaus. Although both bureaus hold a slightly different version of your credit profile, lenders will generally only work with either Equifax or TransUnion.

Wondering why you have more than one credit score? Find out here.

While not all lenders perform credit checks, many will in order to know how trustworthy you’ll be with the loan or other credit product at hand. The better your credit health is, the more likely they’ll be to approve your application, the more credit you can potentially receive, and the more affordable your interest rate will be. This is, of course, why it’s so important to work toward credit improvement in Regina.

Unfortunately, the opposite can occur when you have bad credit. Having unhealthy credit may be due to a number of circumstances, including but not limited to:

- A history of late payments

- Cases of scamming, fraud, or identity theft

- Having too much unpaid, possibly high-interest debt

- A debt consolidation program or debt settlement

- A consumer proposal, bankruptcy, or other delinquency

When you have bad credit, lenders are less inclined to approve your application because they consider you less trustworthy with the money they would be letting you borrow. If you are approved, it will be for a lower credit amount, but a higher interest rate, ultimately costing you more over the life of your credit product.

Your Credit Report and Credit Score

When it comes to your credit health, it’s essential to learn about your credit score and credit report, as they will have a profound impact on your ability to secure credit products down the road. Your credit score and report are also two key components of any credit improvement plan in Regina Saskatchewan, they will provide you with all the details you need to improve and change your financial habits.

Credit Report

As we mentioned, when a lender is considering you for credit, they may perform a credit check through Equifax or TransUnion. They will be looking at your credit report, a detailed personal profile containing all your credit transactions over several years. If they see a history of good payments and other positive points, the outcome for your approval will be good, and vice versa.

Want to know how long information stays on your credit report? Find out here.

Credit Score

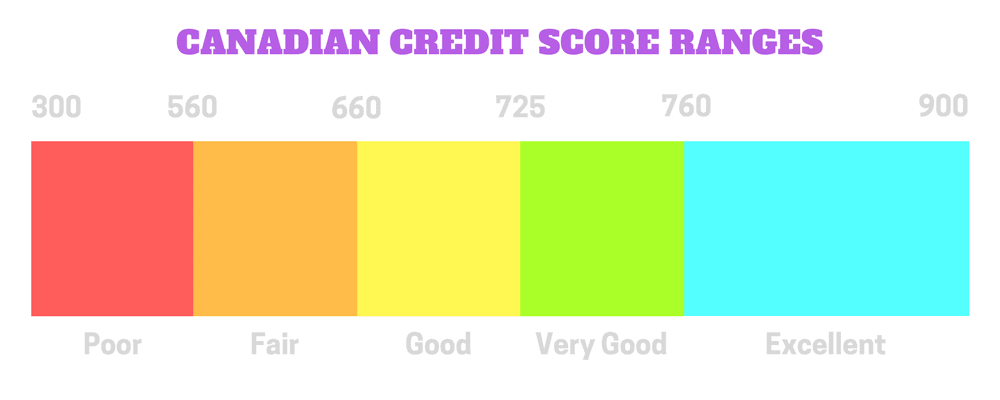

During the check, a lender can also look at your Canadian credit score, a three-digit number ranging from 300-900. Similar to your credit report, your score tells them how good or bad you’ll be at keeping up with payments, only on a more basic level. If they don’t want to go through your entire credit report, your credit score range is a more simple method of determining your creditworthiness.

Good Range (660-900)

This category means you have good credit. Again, this is where your approval odds will go up and your interest rates will go down, leading to the best overall effect on your finances. Since you’re a less risky client, it’s even possible to earn some negotiating power, meaning you may be able to extend or shorten your payment schedule, as well as raise or reduce your payment amounts. If you ever default in some way, your lender may even be willing to forgo any penalties or added interest if you simply explain the situation and continue to be a creditworthy client.

Check out some other surprising perks of having a good credit score.

Fair/Average Range (560-659)

As your credit score drops, your approval odds will lower, but your interest rates will get higher. Point by point, you’ll become a more risky client and the lasting effect on your finances will be worse. Although you still won’t have too much hassle getting approved for a decent amount of credit, you should still be aware that the lower your credit score gets, the more expensive your product will end up being.

Bad Range (300-559)

Here’s when things will become more complicated since lenders will be less trusting and consider you a high-risk client. With a score in this range, the chances of you being approved with a prime lender, such as a bank or credit union, will be slim to none, as their lending regulations are more strict. As such, you may only have success with a private, alternative, or bad credit lender. Budgeting and eventual credit improvement are very important here, as your credit product will have much less affordable interest rates.

Check out this infographic to learn all about the effect of bad credit on your life. How Your Credit Score is Tallied

All this said, if you have bad credit but need to cover some sort of expense right away, it can still be helpful to apply for a bad credit product. In fact, as long as you make all your payments on time and in full, your credit will actually improve gradually. However, if you do have the time to make credit improvements on your own terms, knowing how your credit score is tallied can be helpful.

Essentially, there are 5 main components that affect the way your credit score will be calculated, all of which can be seen in your credit report:

- Payment History (35%) – For obvious reasons, one of the first factors any lender will inspect is your record of payments. Remember, the more on-time payments you make, the better it is for your score, and the more creditworthy you’ll be for it.

- Money Owed (30%) – This factor is especially important when it comes to your revolving debts, such as those from credit cards or lines of credit, but it also applies to loans (non-revolving). The closer you get to maxing out your available credit limit, the lower your score will drop.

- Length of Credit History (15%) – When your score is tallied, the age of your credit accounts will also be analyzed. While it’s not great to have a history of defaulted payments, it’s still better for your score to have a few long-standing accounts in your report, as opposed to many new accounts that you cancel shortly after.

- Applications for New Credit (10%) – Every time you apply for a new credit product, a “hard inquiry” will show up in your report and decrease your score by a few points. That negative effect will last for several months, so it’s best not to apply too many times within a short period, especially if you’re being denied each time.

- Types of Credit Accounts (10%) – Even though you should never take on more credit products than you can handle, it’s good for your credit score to have a variety of product types listed in your report. Of course, results will only be positive if you’re making all your payments in a responsible manner.

Simple Solutions For Credit Improvement in Regina Saskatchewan

As we said, it’s important to improve your credit as much as possible (and as soon as possible) to reduce your financial headaches in the near future. If your credit isn’t too bad yet, you can try some of these simple steps:

- Make any existing payments on time and in full (even for bad credit products)

- Pay off any outstanding debts you might have

- Check your credit report regularly and dispute any errors you find

- Inform both bureaus if you discover any signs of fraud or identity theft

- Start budgeting and cut down on any unnecessary expenses

You’re entitled to one free yearly copy of your credit report from either credit bureau. Here’s how you can get it.

More Drastic Solutions For Credit Improvement

If you already have bad credit and the solutions above are not effective, don’t worry. There are a few more drastic, but equally helpful products you can apply for, including but not limited to:

- Secured credit card

- Credit rehab savings program

- Credit counselling

- Debt settlement

- Debt consolidation loan

- Debt consolidation program

Note: While a debt settlement or a debt consolidation solution may damage your credit temporarily, they can be good alternatives when you have a lot of outstanding unsecured debt that’s already harming your credit health.

Read this to see some of the benefits of a debt consolidation program.

Need a Credit Improvement Solution in Regina?

Living with bad credit in Regina can be a hassle. However, that hassle won’t last long if you contact Loans Canada for a solution. Apply below or get in touch with us today!